Fill Your Et 101 Template

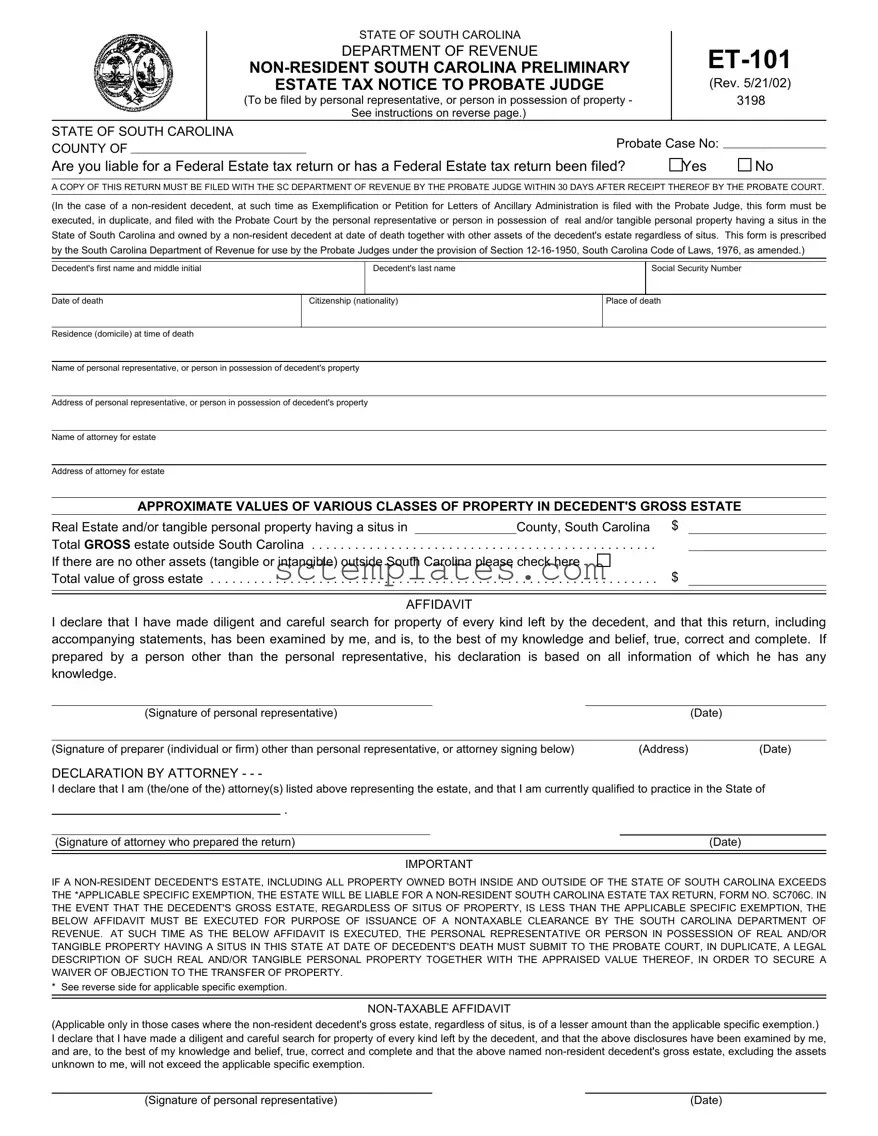

The State of South Carolina takes estate management and taxation seriously, particularly when it comes to assets held within the state by non-residents at the time of their death. This importance is underscored by the requirement for the ET-101 form, a Preliminary Estate Tax Notice that must be filed with the Probate Judge. Specifically designed for non-resident decedents, the ET-101 form serves a key role in ensuring that the estate's holdings are properly reported and taxed in accordance with South Carolina law. This form, not only facilitates the communication between the personal representative (or holder of the decedent's property) and the state's Department of Revenue but also mandates a careful search for and accurate representation of the decedent's assets. Additionally, it includes provisions for both taxable and non-taxable estates based on the value of the estate compared to specific exemption thresholds, which have evolved over time. Key components of the form highlight the necessity of reporting real estate and tangible personal property within South Carolina, alongside comprehensive instructions for filing, deadlines, and conditions under which various affidavits and declarations must be executed. Notably, this form embodies a critical step in ensuring the lawful processing of an estate, guiding personal representatives through the intricacies of state-specific estate taxation, and underscores the state's authority to levy estate taxes in accordance with federal guidelines and individual cases.

Document Example

STATE OF SOUTH CAROLINA

DEPARTMENT OF REVENUE

ESTATE TAX NOTICE TO PROBATE JUDGE

(To be filed by personal representative, or person in possession of property -

See instructions on reverse page.)

(Rev. 5/21/02) 3198

STATE OF SOUTH CAROLINA

COUNTY OF |

|

Probate Case No: |

|

|

|

|

|

|

|

Are you liable for a Federal Estate tax return or has a Federal Estate tax return been filed? |

Yes |

No |

||

A COPY OF THIS RETURN MUST BE FILED WITH THE SC DEPARTMENT OF REVENUE BY THE PROBATE JUDGE WITHIN 30 DAYS AFTER RECEIPT THEREOF BY THE PROBATE COURT.

(In the case of a

Decedent's first name and middle initial |

|

Decedent's last name |

|

|

Social Security Number |

|||

|

|

|

|

|

|

|

|

|

Date of death |

|

Citizenship (nationality) |

|

Place of death |

||||

|

|

|

|

|

|

|

|

|

Residence (domicile) at time of death |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of personal representative, or person in possession of decedent's property |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

Address of personal representative, or person in possession of decedent's property |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

Name of attorney for estate |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address of attorney for estate |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

APPROXIMATE VALUES OF VARIOUS CLASSES OF PROPERTY IN DECEDENT'S GROSS ESTATE |

||||||||

Real Estate and/or tangible personal property having a situs in |

|

County, South Carolina $ |

|

|||||

Total GROSS estate outside South Carolina |

. . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . |

. |

|

|||

If there are no other assets (tangible or intangible) outside South Carolina please check here |

||||||||

Total value of gross estate |

. . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . $ |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

AFFIDAVIT

I declare that I have made diligent and careful search for property of every kind left by the decedent, and that this return, including accompanying statements, has been examined by me, and is, to the best of my knowledge and belief, true, correct and complete. If prepared by a person other than the personal representative, his declaration is based on all information of which he has any knowledge.

(Signature of personal representative) |

|

(Date) |

|

|

|

(Signature of preparer (individual or firm) other than personal representative, or attorney signing below) |

(Address) |

(Date) |

DECLARATION BY ATTORNEY - - -

I declare that I am (the/one of the) attorney(s) listed above representing the estate, and that I am currently qualified to practice in the State of

.

(Signature of attorney who prepared the return) |

(Date) |

|

|

IMPORTANT

IF A

* See reverse side for applicable specific exemption.

(Applicable only in those cases where the

(Signature of personal representative) |

(Date) |

Date of Death |

Applicable Specific Exemption |

||

January 1, 1962 |

- December 31, 1978 |

$60,000 |

|

January 1, 1979 |

- June 30, 1988 |

120,000 |

|

July 1, 1988 |

- June 30, 1989 |

140,000 |

|

July 1, 1989 |

- June 30, 1990 |

170,000 |

|

July 1, 1990 |

- June 30, 1991 |

320,000 |

|

July 1, 1991 |

- thereafter |

same as Federal |

|

Requirement of notice - This notice must be filed with the Probate Judge for the estate of every

Time for filing notice - In the absence of an ancillary administration in this state, the notice must be filed together with exemplifications with the Probate Judge of the county in which the property is located, within 90 days from date of death. If the property is in several counties, file in the county in which the greater part of the property is located, within 90 days after date of death. When an ancillary administration is commenced, the notice must accompany the Petition for Letters of Ancillary Administration.

Persons required to file notice - The duly qualified personal representative, or any person in actual or constructive possession of property included in the statutory gross estate, must file this notice as follows: (1) The personal representative, qualified under an appointment by a court, must file the notice unless at the time of his qualification the notice has already been filed; (2) Any person in actual or constructive possession of property included in the statutory gross estate, must file the notice unless a personal representative qualifies within 3 months after the decedent's death. Persons in actual or constructive possession of such property include custodians, fiduciaries, transferees, joint owners, partners, distributees, debtors, agents, factors, brokers, bankers, safe deposit companies, and warehouse companies.

Signature - The signature of one personal representative is sufficient. If this form is filed by a person other than the personal representative, such person must sign this form and should use a descriptive title such as stated in the last sentence of the above paragraph.

Gross estate - The gross estate, as defined in Section 2031

(a)of the Internal Revenue Code adopted by reference for South Carolina estate tax purposes comprises property of the decedent wherever situated and includes:

1.Property in which the decedent, at the time of his death, has any beneficial interest.

2.Interest of surviving spouse, as dower, curtesy, or estate in lieu thereof.

3.Property transferred by the decedent during his life, by trust or otherwise (other than by bona fide sale for an adequate and full consideration in money or money's worth) as follows: (1) Transfers intended to take effect in possession or enjoyment at or after the decedent's death; (2) Transfers under which the decedent reserved or retained (in whole or in part) the use, possession, rents, or other income or enjoyment of the transferred property, for his life, or for a period not ascertainable without reference to his death, or for a period of such duration as to evidence an intention that it should extend to his death; (3) Transfers under which the decedent retained the right, either alone or in conjunction with another person or persons, to designate who should possess or enjoy the property or the income therefrom; and (4) Transfers under which the enjoyment of the transferred property was subject at decedent's death to a change through the exercise, either by the decedent alone or in conjunction with another person or persons, of a power to alter, amend, revoke or terminate.

4.Annuities received by any beneficiary by reason of surviving the decedent.

5.Property owned jointly or in tenancy with right of survivorship.

6.Property subject to a general power of appointment, including property with respect to which the decedent exercised or released the power during his lifetime.

7.Insurance upon the life of the decedent, including insurance receivable by beneficiaries other than the estate.

For decedents dying on or after July 1, 1991: South Carolina has adopted the Internal Revenue Code Section 2011. The term "Federal Credit" means the maximum amount of the credit for state death taxes allowable by the Internal Revenue Code Section 2011. The term "maximum amount" must be construed so as to take full advantage of the credit as allowed by the Internal Revenue Code.

Lien - A lien upon the property of a

Penalties - Penalties are provided for under Chapter 54 of Title 12.

Form Properties

| Fact | Detail |

|---|---|

| Form Title | Non-Resident South Carolina Preliminary Estate Tax Notice to Probate Judge |

| Form Number | ET-101 |

| Last Revision | May 21, 2002 |

| Governing Law | Section 12-16-1950, South Carolina Code of Laws, 1976, as amended |

| Purpose | To be filed by a personal representative or person in possession of property for non-resident decedents having property in South Carolina |

| Submission Requirement | A copy must be filed with the SC Department of Revenue by the Probate Judge within 30 days after receipt by the Probate Court |

| Estate Tax Liability Consideration | If a non-resident decedent's estate exceeds the applicable specific exemption, it is liable for a non-resident South Carolina Estate Tax Return, Form No. SC706C |

| Applicable Specific Exemptions | Varying exemption amounts based on the date of death, aligning with federal requirements post-July 1, 1991 |

| Filing Timeframe | Within 90 days from the date of death, adjusted for ancillary administrations or property across multiple counties |

| Entities Required to File | Qualified personal representatives or any person in actual or constructive possession of the decedent's property |

| Key Components of Gross Estate | Includes real estate, tangible and intangible personal property regardless of location, and other specified assets |

Guide to Writing Et 101

Filling out the ET-101 form is a critical step for personal representatives or individuals in possession of property belonging to a non-resident decedent with property in South Carolina. This form acts as a preliminary estate tax notice to the Probate Judge and is necessary for ensuring all estate tax responsibilities are correctly addressed. Its completion allows the South Carolina Department of Revenue to assess whether estate taxes are due for the property within the state. Carefully follow the steps below to ensure the form is completed accurately and complently.

- Start by entering the county in South Carolina where the form is being filed at the top of the document.

- Fill in the Probate Case No., if available.

- Indicate whether a Federal Estate tax return is liable to be filed or has been filed by checking "Yes" or "No".

- Enter the decedent's first name, middle initial, and last name, as well as their Social Security Number.

- Provide the date and place of the decedent's death, including their citizenship (nationality) and their residence (domicile) at the time of death.

- Write the name and address of the personal representative, or person in possession of the decedent's property.

- Include the name and address of the attorney for the estate, if applicable.

- Under the section for APPROXIMATE VALUES OF VARIOUS CLASSES OF PROPERTY, enter the values for real estate and/or tangible personal property in South Carolina, the total gross estate outside South Carolina, and check the box if there are no other assets outside South Carolina.

- Total the value of the gross estate and input the value.

- The Affidavit section must be signed by the personal representative, declaring diligent search for property and verifying the accuracy of the document. Include the preparer's signature, address, and date if prepared by someone other than the personal representative.

- If there is an attorney who prepared the return, they must complete the Declaration by Attorney section, including their signature, date, and stating their qualification to practice in the state.

- For estates of non-resident decedents not exceeding the specific exemption, fill in the NON-TAXable Affidavit section, declaring diligent search and attesting to the estate's value relative to the specific exemption, followed by the personal representative's signature and date.

- Refer to ET-101 Instructions for guidance on the applicable specific exemption based on the date of death and additional details on completing the form.

Upon completing the ET-101 form, it's important to submit it in duplicate to the relevant Probate Court within the timelines specified in the instructions. Remember to also prepare and attach any supplemental documents that may be required, such as legal descriptions of real and/or tangible personal property within South Carolina. This will ensure that all legal requirements for reporting and assessing estate taxes for non-resident decedents are fully met.

Understanding Et 101

What is the ET-101 form in South Carolina?

The ET-101 form, also known as the Non-Resident South Carolina Preliminary Estate Tax Notice to Probate Judge, is a document that must be filed by the personal representative or a person in possession of property belonging to a non-resident decedent's estate. This form is necessary for the South Carolina Department of Revenue to assess the need for estate tax filing and determines the estate's liability for taxes within the state.

Who is required to file the ET-101 form?

The ET-101 form must be filed by the personal representative appointed by the court or any person who is in actual or constructive possession of any real and/or tangible personal property located in South Carolina and owned by a non-resident decedent at the time of death. This includes custodians, fiduciaries, transferees, joint owners, partners, distributees, debtors, agents, and similar roles.

When should the ET-101 form be submitted?

The submission timeline for the ET-101 form depends on whether there is an ancillary administration in South Carolina. If there is no ancillary administration, it should be filed with the Probate Judge within 90 days from the date of death. Should there be an ancillary administration, it must accompany the Petition for Letters of Ancillary Administration.

Is there a penalty for not filing the ET-101 form on time?

Yes, the State of South Carolina may impose penalties for failure to file the ET-101 form within the designated timeframe. These penalties are outlined under Chapter 54 of Title 12 of the South Carolina Code of Laws and can include fines or other legal consequences.

What information is needed to complete the ET-101 form?

To complete the ET-101 form, one needs to provide detailed information about the decedent, including their full name, Social Security Number, date of death, citizenship, and place of death. Additionally, information about the personal representative or person in possession of the decedent's property, attorney for the estate if applicable, and an approximate value of the decedent's gross estate must be included.

How is the "gross estate" defined for the purposes of the ET-101 form?

The gross estate of a decedent encompasses all property owned at the time of death, including real estate and tangible personal property located in South Carolina, and is defined in alignment with Section 2031(a) of the Internal Revenue Code. It considers property the decedent had a beneficial interest in, jointly owned property, and property transferred by the decedent before death but with retained interest or control, among others.

What happens if the decedent's estate does not exceed the applicable specific exemption?

If the non-resident decedent's gross estate, including all property regardless of its location, does not exceed the specific exemption amounts relevant to the date of death, then the estate may not be liable for estate taxes in South Carolina. In this case, a non-taxable affidavit must be executed and filed for the issuance of a non-taxable clearance by the South Carolina Department of Revenue.

Are copies of the ET-101 form required to be sent elsewhere?

Yes, a copy of the ET-101 form must be filed with the South Carolina Department of Revenue by the Probate Judge within 30 days after they receive it from the personal representative or other individual filing the notice.

Where can I find the applicable specific exemption amounts for different dates of death?

The applicable specific exemption amounts vary depending on the date of death of the decedent and are listed on the reverse side of the ET-101 form. These amounts have historically ranged from $60,000 for deaths occurring before December 31, 1978, to amounts equivalent to the federal exemptions for deaths after July 1, 1991.

Common mistakes

Failing to report all assets accurately is a common mistake made by individuals when completing the ET-101 form. The form requires a detailed account of the decedent’s gross estate, including real estate and tangible personal property located in South Carolina, as well as assets located outside the state. Often, inaccuracies arise from an oversight or misunderstanding of what constitutes the gross estate. These inaccuracies can stem from underreporting, overlooking certain assets, or misinterpreting the form's instructions regarding the inclusion of all relevant property.

Another frequent error is the incorrect identification of the decedent's domicile at the time of death. This information is crucial, as the ET-101 form is specifically designed for non-resident decedents. The domicile of the decedent determines the applicable estate tax rules and exemptions. Mistakes in this area might result from confusion about the legal definition of domicile, especially if the decedent lived in multiple places or moved frequently near the end of life.

Failure to provide complete information for the personal representative or the person in possession of the decedent’s property is also common. The ET-101 form requires the name and address of the personal representative or the individual responsible for the property. Sometimes, people filling out the form might leave these sections incomplete either because they are waiting for the official appointment of a personal representative or due to a lack of understanding of who qualifies as a person in possession of the decedent’s property.

Lastly, many individuals fail to attach necessary documentation or complete all required affirmations and declarations. The ET-101 form mandates the attachment of certain documents, such as a copy of the return to be filed with the South Carolina Department of Revenue and, in some cases, legal descriptions of real and/or tangible personal property located in South Carolina. Additionally, the form includes sections for affidavits and declarations by both the personal representative and the attorney, which are often overlooked or improperly executed due to oversight or unfamiliarity with the procedural requirements.

Documents used along the form

When dealing with estate matters, especially concerning non-resident decedents in the state of South Carolina, several forms and documents often accompany the ET-101 form, STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE NON-RESIDENT SOUTH CAROLINA PRELIMINARY ESTATE TAX NOTICE TO PROBATE JUDGE. These forms and documents are crucial for a comprehensive approach to estate management and compliance with legal obligations. Understanding each document's purpose can significantly streamline the process for personal representatives or individuals in possession of the decedent's property.

- SC706C Non-Resident South Carolina Estate Tax Return: This form is necessary if the non-resident decedent's estate exceeds the applicable specific exemption amount. It details the estate's taxable assets and calculates the estate tax due to South Carolina.

- Probate Court Petition for Letters of Ancillary Administration: Required to initiate ancillary probate proceedings in South Carolina, this petition seeks the appointment of an executor or administrator to manage the estate's assets within the state.

- Inventory and Appraisement Form: An essential document for estate administration, this form lists all assets in the decedent's estate, including those located in South Carolina, and assigns values to them, facilitating estate valuation and tax calculations.

- Death Certificate: This official document certifies the death of the individual, stating the date, location, and cause of death. It's necessary for all proceedings related to the decedent's estate.

- Legal Description of Real and/or Tangible Personal Property: This detailed description of real estate and tangible property within South Carolina is required for a waiver of objection to the transfer of property and for estate tax purposes.

- Affidavit of Diligent Search: This affidavit attests that the personal representative or individual in possession of the decedent's property has conducted a thorough search for all assets, ensuring that the estate inventory is complete and accurate.

- Waiver of Objection to Transfer of Property: This document, often a formality in estate settlement, indicates that there are no legal objections to the transfer of the listed property from the decedent to the inheritors.

- Receipts and Releases Form: This form documents the distribution of estate assets to the beneficiaries or heirs and their acknowledgement of receiving their rightful shares, often required to close the estate in probate.

Managing an estate, particularly for non-resident decedents, involves a complex interplay of legal requirements and documentation. Each of the above-stated forms and documents plays a vital role in ensuring compliance with South Carolina's estate laws and facilitating the smooth execution of the decedent's final affairs. Personal representatives and others involved in estate management should familiarize themselves with these documents to navigate the process effectively.

Similar forms

The ET-101 form is closely related to the Federal Estate Tax Return (Form 706), as it deals with the estate of a deceased person. The Federal Estate Tax Return is required for reporting the decedent's estate value and determining the federal estate tax due. Both forms are used to assess the estate's tax liability, but while the ET-101 focuses on non-resident decedents with property in South Carolina, Form 706 applies to estates that may have a federal tax liability based on the total value of the estate.

Similar to the ET-101, the Affidavit for Collection of Personal Property (Form 5) is utilized in the probate process but on a much smaller scale. Form 5 is designed for small estates that can bypass the formal probate process. Although this form simplifies asset collection, both it and the ET-101 require detailed information about the decedent's assets to facilitate legal transfer and taxation adherence.

The Application for Estate Tax Clearance Certificate is another document akin to the ET-101. This application seeks confirmation that all estate tax liabilities have been cleared before assets are distributed to beneficiaries. While the ET-101 notifies the probate judge about the decedent’s assets' status within South Carolina for tax purposes, the Estate Tax Clearance Certificate ensures that the estate has settled its tax responsibilities, safeguarding the estate from future claims.

The Real Property Transfer on Death (TOD) deed closely resembles the ET-101 in intention but operates differently. A TOD deed allows property owners to name beneficiaries to their real estate to avoid probate upon their death. While the ET-101 deals with the tax implications of already transferred estate property, the TOD deed is a proactive measure, avoiding complications by delineating ownership beforehand.

The Ancillary Probate Application is another form that corresponds with the ET-101, particularly for estates extending across different jurisdictions. When a decedent owns property in a state other than their domicile, an ancillary probate process is necessary alongside the primary probate proceeding. The ET-101 addresses issues related to non-resident decedents in South Carolina, similar to how an ancillary probate application would facilitate legal proceedings in another state.

The Petition for Letters of Administration is used when an estate requires administration but there's no will. This petition requests the appointment of an administrator to manage the deceased's estate, paralleling the ET-101's requirement for a personal representative or holder of the decedent’s property to file the document. Both are pivotal in the initiation phase of estate processing, ensuring legal clarity and proceeding with asset management and tax obligations.

The Non-Taxable Affidavit operates similarly to the ET-101 for estates that fall under a specific exemption threshold, indicating no estate tax is due. While the Non-Taxable Affidavit directly claims an estate tax exemption based on its value, the ET-101 may also lead to declaring an estate non-taxable if the asset valuation falls below South Carolina's taxable limits. Both documents are essential for clarifying the tax responsibilities of an estate.

Dos and Don'ts

When dealing with the ET-101 form for the State of South Carolina, it's crucial to approach this document with careful attention to detail. Here’s a guide to what you should and shouldn't do:

Do:- Read the instructions carefully before you start filling out the form. Understanding the requirements can save you from making mistakes.

- Gather all the necessary documents related to the decedent's estate beforehand. This information will be vital in accurately completing the form.

- Double-check all entries for accuracy, especially figures related to the estate's value and personal information. Errors can lead to delays or issues with the South Carolina Department of Revenue.

- File the form within the specified time frame. Submitting the ET-101 form to the Probate Judge in a timely manner is crucial to avoid penalties.

- Overlook property situated outside of South Carolina. Even though the form is for a non-residential estate, it also requires information on assets located outside the state.

- Forget to sign and date the form. An unsigned form is equivalent to not filing at all, and this can result in unnecessary complications.

- Assume the value of the estate without a proper appraisal. Approximations can lead to incorrect taxation or other legal challenges.

- Ignore the need for a legal description of real and/or tangible personal property within South Carolina. This information is essential for the ET-101 form and must be precise.

Misconceptions

When dealing with the South Carolina Department of Revenue's ET-101 form, also known as the Non-Resident South Carolina Preliminary Estate Tax Notice, individuals often fall prey to a number of misconceptions. Addressing these misconceptions is key to ensuring that personal representatives or those in possession of a non-resident decedent's property navigate the estate process correctly. Here are seven common misconceptions about the ET-101 form and the truths behind them:

- Misconception: The ET-101 form is only for residents of South Carolina.

Truth: The ET-101 form is specifically designed for non-residents of South Carolina. It applies when a non-resident decedent owned real and/or tangible personal property within the state at the time of death.

- Misconception: Filing the ET-101 form is optional.

Truth: Filing the ET-101 form is mandatory for the personal representative or anyone in possession of the decedent’s property within South Carolina. It must be filed with the Probate Judge within 30 days after receipt by the Probate Court.

- Misconception: There’s no deadline for filing the ET-101 form.

Truth: There is a deadline for filing the ET-101 form. It must be filed within 90 days from the date of the decedent's death or at the time of filing for ancillary administration, if applicable.

- Misconception: The ET-101 form covers the entirety of the estate process.

Truth: The ET-101 form is a preliminary notice. It may lead to further obligations such as the filing of a non-resident South Carolina estate tax return (Form SC706C) if the estate's value exceeds the applicable specific exemption.

- Misconception: Any asset owned outside of South Carolina does not need to be reported.

Truth: While the ET-101 focuses on property within South Carolina, the form requires information about the total gross estate, which includes assets outside the state. If there are no other assets outside South Carolina, a specific box must be checked on the form.

- Misconception: Only the personal representative can sign the ET-101 form.

Truth: The ET-101 form can be signed by the personal representative or an individual acting on behalf of the representative. If prepared by someone other than the personal representative, that person's declaration of accuracy is required.

- Misconception: A non-taxable affidavit is always required with the ET-101 form.

Truth: The non-taxable affidavit is only necessary if the non-resident decedent’s gross estate, excluding any assets unknown to the filer, falls below the applicable specific exemption. This affidavit is crucial for obtaining a nontaxable clearance.

Understanding these key points ensures that the ET-101 form is filled out and submitted correctly, aiding in the smooth administration of a non-resident's estate in South Carolina.

Key takeaways

Understanding the ET-101 form is crucial for non-resident estate representatives in South Carolina. Here are four key takeaways about filling out and utilizing this form:

- Filing Requirement: The ET-101 form, a Preliminary Estate Tax Notice, must be filed by the personal representative or anyone in possession of the decedent's property. This step is essential for non-residents who owned property in South Carolina at the time of their death. The necessity to file applies regardless of the property's value or the estate's overall gross worth.

- Deadline for Submission: It's important to adhere to the specified deadlines. The form, along with a copy of the Federal Estate Tax Return if applicable, needs to be submitted to the South Carolina Department of Revenue by the Probate Judge within 30 days of receipt. If there's no ancillary administration in the state, directly filing it with the Probate Judge in the county where the property is located, within 90 days of the decedent's death, becomes necessary.

- Details Required: Completeness and accuracy in the ET-101 form are paramount. The form requires detailed information about the decedent, including their full name, social security number, date and place of death, as well as citizenship. It also requires comprehensive data regarding the estate's assets, specifically real estate and tangible personal property located in South Carolina and a declaration concerning the gross estate's total value.

- Affidavit Verification: An affidavit section at the bottom part of the form necessitates a declaration from the personal representative. It serves as a confirmation that a diligent search for the decedent's property was conducted and that the information provided in the form is, to the best of the preparer's knowledge and belief, true, correct, and complete. This affirmation ensures accountability and the integrity of the information submitted.

Understanding these key aspects of the ET-101 form can significantly ease the process for those handling non-resident estate matters in South Carolina, ensuring compliance with state requirements and helping facilitate the tax assessment process for such estates.

More PDF Templates

Form 1120s 2022 - The form's instructions highlight the necessity of including the business name, FEIN, and SC File Number for identification purposes.

Sc Dss Forms - Ensure continuous ADAP insurance benefits by completing the insurance recertification process.