Fill Your I 295 Template

In navigating the complexities of real estate transactions within South Carolina, the I-295 form emerges as a critical document, especially for nonresident sellers. At its core, it serves as a seller's affidavit, instrumental in the withholding tax obligations that arise during property sales. The State of South Carolina, through its Department of Revenue, mandates this affidavit under the guidance of S.C. Code Section 12-8-580 and SC Revenue Ruling #09-13, underscoring its significance in ensuring tax compliance. A deeper dive into the form reveals it is not merely bureaucratic paperwork but a structured declaration by the seller regarding the sale’s specifics, from property descriptions to the anticipated closing date. It delineates responsibilities concerning South Carolina income tax returns, clearly addresses exemptions, and even navigates through scenarios of resident and non-resident status definitions per state tax laws. In scenarios involving more nuanced sales, like those under the installment sale method or in the context of like-kind exchanges, the I-295 form provides a pathway to transparency and compliance. Furthermore, this affidavit touches on tax considerations for particular circumstances, such as sales not subject to tax due to principal residence sales or involuntary conversions. By setting out these declarations and attachments, the form helps sellers articulate their tax obligations and exemptions, thereby informing the withholding process and safeguarding both parties against potential legal pitfalls. For individuals embarking on the sale of real estate within this jurisdiction, understanding and accurately completing this affidavit is instrumental in navigating the procedural and legal complexities of such transactions.

Document Example

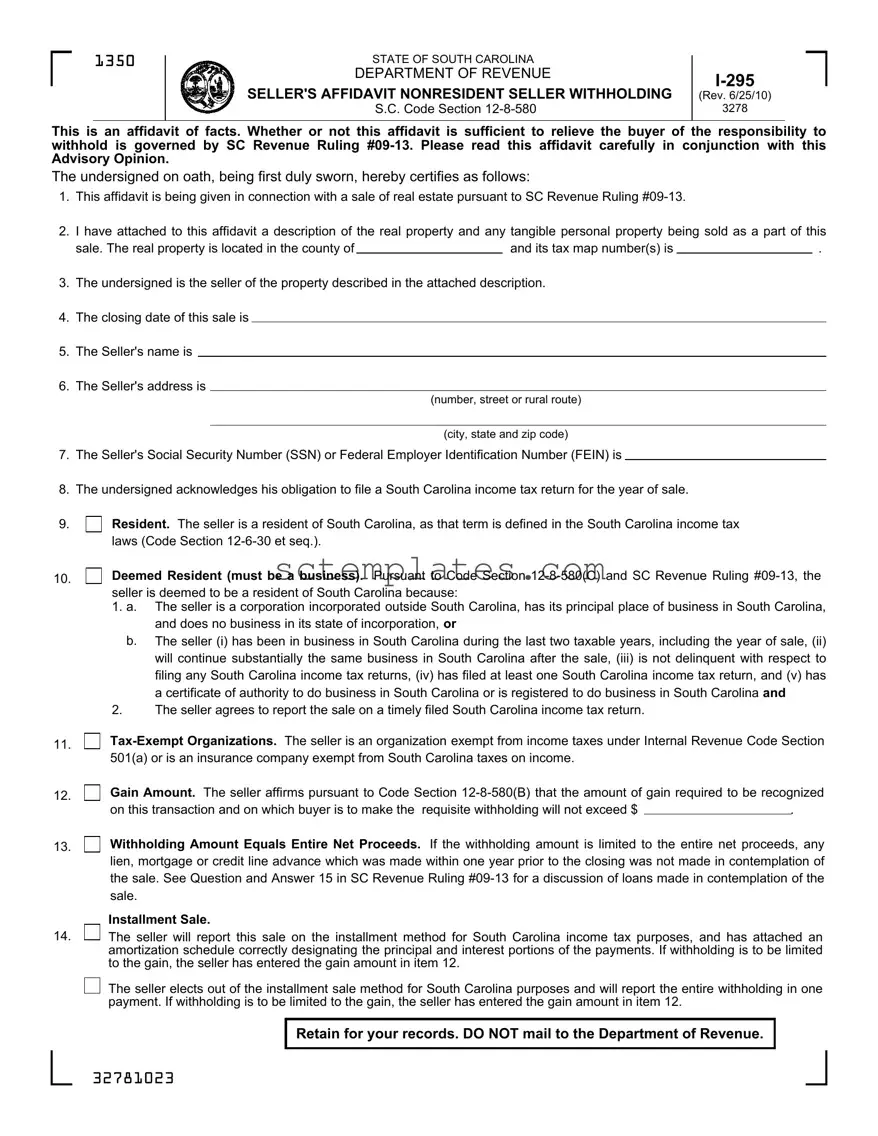

1350

STATE OF SOUTH CAROLINA

DEPARTMENT OF REVENUE

SELLER'S AFFIDAVIT NONRESIDENT SELLER WITHHOLDING

S.C. Code Section

(Rev. 6/25/10)

3278

This is an affidavit of facts. Whether or not this affidavit is sufficient to relieve the buyer of the responsibility to withhold is governed by SC Revenue Ruling

The undersigned on oath, being first duly sworn, hereby certifies as follows:

1.This affidavit is being given in connection with a sale of real estate pursuant to SC Revenue Ruling

2.I have attached to this affidavit a description of the real property and any tangible personal property being sold as a part of this

sale. The real property is located in the county of |

|

and its tax map number(s) is |

|

. |

3.The undersigned is the seller of the property described in the attached description.

4.The closing date of this sale is

5.The Seller's name is

6.The Seller's address is

(number, street or rural route)

(city, state and zip code)

7.The Seller's Social Security Number (SSN) or Federal Employer Identification Number (FEIN) is

8.The undersigned acknowledges his obligation to file a South Carolina income tax return for the year of sale.

9.

10.

11.

12.

13.

14.

Resident. The seller is a resident of South Carolina, as that term is defined in the South Carolina income tax laws (Code Section

Deemed Resident (must be a business). Pursuant to Code Section

1.a. The seller is a corporation incorporated outside South Carolina, has its principal place of business in South Carolina, and does no business in its state of incorporation, or

b.The seller (i) has been in business in South Carolina during the last two taxable years, including the year of sale, (ii) will continue substantially the same business in South Carolina after the sale, (iii) is not delinquent with respect to filing any South Carolina income tax returns, (iv) has filed at least one South Carolina income tax return, and (v) has a certificate of authority to do business in South Carolina or is registered to do business in South Carolina and

2.The seller agrees to report the sale on a timely filed South Carolina income tax return.

Gain Amount. The seller affirms pursuant to Code Section

on this transaction and on which buyer is to make the requisite withholding will not exceed $ |

. |

|

|

|

|

Withholding Amount Equals Entire Net Proceeds. If the withholding amount is limited to the entire net proceeds, any lien, mortgage or credit line advance which was made within one year prior to the closing was not made in contemplation of the sale. See Question and Answer 15 in SC Revenue Ruling

Installment Sale.

The seller will report this sale on the installment method for South Carolina income tax purposes, and has attached an amortization schedule correctly designating the principal and interest portions of the payments. If withholding is to be limited to the gain, the seller has entered the gain amount in item 12.

The seller elects out of the installment sale method for South Carolina purposes and will report the entire withholding in one payment. If withholding is to be limited to the gain, the seller has entered the gain amount in item 12.

Retain for your records. DO NOT mail to the Department of Revenue.

32781023

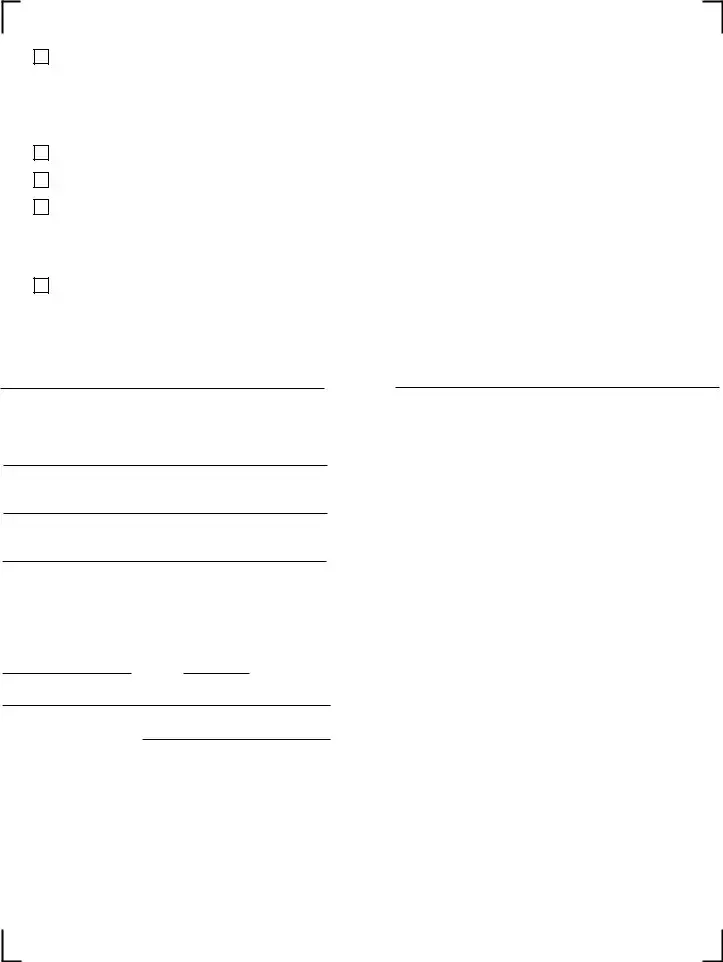

15.

Principal Residence or Involuntary Conversion - Nonrecognition of Gain. The sale of the property will not be subject to taxes because of Internal Revenue Code Section 121 (sale of a principal residence) or Internal Revenue Code Section 1033 (involuntary conversions.) If the seller fails to comply with Section 1033, the seller acknowledges an obligation to file an amended South Carolina income tax return for the year of the sale.

16.

17.

Like Kind Exchange.

In a simultaneous exchange, the entire gain is deferred under Internal Revenue Code Section 1031.

A gain will be partially recognized. Enter the gain amount in item 12.

The gain is intended to be deferred under Internal Revenue Code Section 1031 using a qualified intermediary and the steps required by SC Revenue Ruling

Employee Relocation. The transaction involves the sale of an employee's property which is being sold by an employer or relocation company in connection with the employee's transfer. For income tax purposes the sale is treated as a sale by the employer or relocation company.

The undersigned understands that this affidavit may be disclosed to the Department and that any false statement contained herein could be punished by fine, imprisonment, or both.

(Signature) |

(Name - Please Print) |

If the person making the affidavit is not the Seller, complete the following:

(Affiant's SSN or FEIN)

(Affiant's number, street or rural route)

(Affiant's city, state and zip code)

SUBSCRIBED AND SWORN to

Before me this |

|

day of |

|

, year of

(Notary Public)

My Commission Expires:

Social Security Privacy Act Disclosure

It is mandatory that you provide your social security number on this tax form if you are an individual taxpayer. 42 U.S.C 405(c)(2)(C)(i) permits a state to use an individual's social security number as means of identification in administration of any tax. SC Regulation

The Family Privacy Protection Act

Under the Family Privacy Protection Act, the collection of personal information from citizens by the Department of Revenue is limited to the information necessary for the Department to fulfill its statutory duties. In most instances, once this information is collected by the Department, it is protected by law from public disclosure. In those situations where public disclosure is not prohibited, the Family Privacy Protection Act prevents such information from being used by third parties for commercial solicitation purposes.

Our Internet address is: www.sctax.org

32782021

Form Properties

| Fact | Detail |

|---|---|

| Governing Law | South Carolina Code Section 12-8-580; SC Revenue Ruling #09-13 |

| Purpose | The form serves as an affidavit of facts related to the sale of real estate by a nonresident seller. |

| Responsibility for Withholding | The affidavit may relieve the buyer of the responsibility to withhold taxes if conditions are met as per SC Revenue Ruling #09-13. |

| Key Requirements for the Seller | Sellers must provide a detailed description of the property, confirm their status (resident, nonresident, or deemed resident), acknowledge the obligation to file a South Carolina income tax return, and, if applicable, report the sale and any gains. |

| Special Conditions | Includes provisions for tax-exempt organizations, installment sales, principal residence or involuntary conversion exclusions, like-kind exchanges, and employee relocations. |

Guide to Writing I 295

Upon preparing to fill out the I-295 form, also known as the Seller's Affidavit Nonresident Seller Withholding, according to the State of South Carolina Department of Revenue, it's crucial to thoroughly understand the document and its accompanying directives, notably SC Revenue Ruling #09-13. This affidavit serves as a testimony of facts pertinent to the sale of real estate by a nonresident seller within South Carolina. Completion of this form is a detailed process, necessitating accurate and comprehensive information about the sale, the seller, and the property involved. Below are the explicit steps to fill out the form correctly.

- Start by reading SC Revenue Ruling #09-13 carefully to understand the conditions under which the buyer can be relieved from the withholding requirement.

- Enter the affidavit date and your full legal name at the beginning of the form where indicated.

- Attach a detailed description of the real property and any tangible personal property included in the sale. Include the property's location by county and its tax map number(s).

- State your relationship to the property, confirming that you are the seller of the described property.

- Fill in the closing date of the property sale.

- Provide your full name as the seller in the space provided.

- Input your complete address, including number, street, city, state, and zip code.

- Enter your Social Security Number (SSN) or Federal Employer Identification Number (FEIN).

- Acknowledge your obligation to file a South Carolina income tax return for the year of the sale.

- If applicable, indicate that you are a resident of South Carolina or meet the conditions of being deemed a resident for the purpose of this transaction.

- For tax-exempt organizations or if subject to special tax conditions like an installment sale or like-kind exchange, provide the relevant information as per the form's requirements.

- If limiting withholding to the gain or the entire net proceeds, specify the amounts as necessitated by the transaction details.

- For properties not subject to taxes due to specific conditions like principal residence sale or involuntary conversion, make the necessary declarations.

- If the form is being filled out by someone other than the seller, provide the affiant's information, including name, SSN or FEIN, address, and contact details.

- Sign and date the form in the presence of a Notary Public, ensuring the notary completes their section, including their commission expiration date.

After completing the I-295 form, remember that this document is for record-keeping and should be retained accordingly. It is not required to be mailed to the Department of Revenue. However, accuracy and truthfulness in filling out this form are critical as any false statement could lead to legal penalties. Moreover, it is essential to keep a copy of this affidavit, along with all attachments and related documentation, as part of your records related to the sale.

Understanding I 295

What is the I-295 form?

The I-295 form, also known as the Seller's Affidavit Nonresident Seller Withholding, is a legal document used by the State of South Carolina Department of Revenue. It serves to provide information regarding the sale of real estate by nonresident sellers and outlines the seller's obligations concerning withholding taxes as per South Carolina Code Section 12-8-580 and SC Revenue Ruling #09-13. It must be filled out and signed by the seller involved in the real estate transaction.

Who needs to fill out the I-295 form?

Nonresident sellers of real estate in South Carolina are required to complete the I-295 form. This includes individuals, corporations, tax-exempt organizations, and insurance companies selling property within the state who do not reside in South Carolina.

What purpose does the I-295 form serve?

The form is used to affirm the seller's residency status, obligation to file a South Carolina income tax return, and provide details concerning the sale of real property. It essentially assists in the correct withholding and reporting of taxes due from the proceeds of real estate transactions, ensuring compliance with state tax laws.

What information is required on the I-295 form?

Sellers need to provide a detailed account of the real estate sale, including property description, closing date, seller's name, address, Social Security Number (SSN) or Federal Employer Identification Number (FEIN), residency status, and acknowledgment of tax obligations. Additionally, the form requires details about the transaction's gain amount, any tax-exempt status of the seller, installment sale agreements, and special circumstances like principal residence sales or like-kind exchanges.

How does a seller certify their residency status on the I-295 form?

A seller can certify their residency status as a resident, a deemed resident (in cases where businesses are involved), or a nonresident based on specific criteria outlined in the South Carolina income tax laws and SC Revenue Ruling #09-13. Detailed conditions under each category must be met and accurately represented in the affidavit.

What are the implications for a seller deemed a tax-exempt organization?

Tax-exempt organizations, as defined under Internal Revenue Code Section 501(a) or insurance companies exempt from South Carolina taxes, need to declare their tax-exempt status on the I-295 form. This declaration affects the withholding requirements for the sale, possibly reducing or eliminating the obligation to withhold taxes from the sale proceeds.

What does the I-295 form stipulate about the gain on property sales?

The form requires sellers to affirm the gain amount required to be recognized from the property transaction, which directly influences the withholding amount the buyer must reserve for tax purposes. Accurate calculation and reporting of the gain are crucial for compliance with tax withholding requirements.

Are there special sections for specific types of property sales, like principal residence or like-kind exchanges?

Yes, the I-295 form includes provisions for sellers to report sales involving a principal residence, which may qualify for nonrecognition of gain under Internal Revenue Code Section 121, and for properties sold in like-kind exchanges under Internal Revenue Code Section 1031. These sections are intended to ensure that sellers take advantage of applicable tax exemptions or deferrals correctly.

What happens if the information provided on the I-295 form is found to be false?

Falsifying information on the I-295 form is a serious offense that can lead to penalties, including fines or imprisonment. Sellers are reminded that they are under oath when providing information on this affidavit, underscoring the importance of accuracy and truthfulness in their disclosures.

Common mistakes

Not attaching a detailed description of both the real property and any tangible personal property being sold as part of the sale. This can create confusion and is necessary for a complete submission.

Failure to accurately indicate the property's tax map number(s). This number is crucial for identifying the property within county records.

Incomplete seller information, such as omitting the seller’s full name or providing an incomplete address. Accurate and full identification is required to process the affidavit correctly.

Incorrect or missing Social Security Number (SSN) or Federal Employer Identification Number (FEIN). This is a common oversight that can significantly delay processing.

Omitting the closing date of the sale. This date is essential for tax purposes and to confirm the timing of the sale.

Not acknowledging the obligation to file a South Carolina income tax return for the year of sale. This acknowledgment is a critical declaration of the seller's tax responsibilities.

Failing to specify whether the seller is a resident, deemed resident, or tax-exempt organization. This information affects tax obligations and the need for withholding.

Leaving the gain amount blank or incorrectly calculating it. This figure is essential for determining the correct withholding amount.

Not considering special situations such as installment sale, like-kind exchange, or employee relocation. Each requires specific declarations and documentation.

Each of these mistakes can be avoided by thoroughly reviewing the I-295 form instructions and consulting with a professional if necessary. Attention to detail is critical.

Using clear, legible handwriting or typing the information can prevent misunderstandings or delays.

Double-check all entries for accuracy before submitting the form. Errors can lead to unnecessary complications or legal issues down the road.

Documents used along the form

When dealing with real estate transactions, particularly from a nonresident perspective in South Carolina, the I-295 form, or the Seller's Affidavit Nonresident Seller Withholding, plays a crucial role. However, this form rarely acts alone in fulfilling the requirements and safeguards necessary for a smooth transaction. Several additional forms and documents often supplement the I-295 form to ensure compliance with all statutes and to facilitate a well-documented transfer of property. Among these, the following four documents are routinely used.

- Closing Disclosure: This form provides a detailed account of the financial transactions involved in a real estate deal. It breaks down the costs paid by the buyer and the seller, including the escrow, agent fees, lender charges, and any other transaction costs or credits. It’s crucial for ensuring that both parties are fully aware of, and agree to, the financial details of the transaction.

- 1099-S Form: This document is vital for reporting the proceeds from real estate transactions to the IRS. For nonresident sellers, it's essential to demonstrate compliance with U.S. tax law, specifically regarding capital gains taxes. It effectively declares the amount obtained from the sale of the property.

- Non-Foreign Affidavit under FIRPTA: The Foreign Investment in Real Property Tax Act requires a statement from sellers to assert they are not foreign persons. This legal assertion is critical in transactions involving nonresident sellers as it affects the withholding requirements. It provides assurance to the buyer and the IRS that the seller is subject to U.S. taxes.

- State Return for Nonresident Sellers: This document is a state-specific tax return for nonresident sellers to declare income or gains derived from the sale of property within the state. For South Carolina, this ensures that the nonresident seller complies with state tax laws regarding income from the sale, coinciding with the attestation made in the I-295 form.

Understanding and utilizing these documents in conjunction with the I-295 form ensures compliance with both state and federal laws, providing a safeguard for all parties involved in the transaction. It is not merely about fulfilling legal requirements but also about ensuring trust and transparency between buyers and sellers, pivotal for the integrity of real estate transactions involving nonresident sellers in South Carolina.

Similar forms

The I-295 Seller's Affidavit Nonresident Seller Withholding is closely related to the IRS Form 8288, U.S. Withholding Tax Return for Dispositions by Foreign Persons of U.S. Real Property Interests. Both forms are designed to ensure compliance with tax obligations related to the sale of real estate. The I-295 form specifically applies to nonresident sellers in South Carolina, requiring them to declare their tax status and assure they meet specific withholding requirements, similar to how Form 8288 requires foreign persons to report income and withholding related to the sale of U.S. real property.

Another document akin to the I-295 form is the IRS Form 1099-S, Proceeds From Real Estate Transactions. This form is used to report the sale or exchange of real estate and is pertinent for both residential and commercial transactions. While Form 1099-S is more focused on the reporting of proceeds to the IRS and to the person selling the property, the I-295 form is specifically concerned with the affidavit of nonresident sellers regarding their withholding obligations, highlighting their complementary roles in real estate transaction reporting.

The Nonresident Alien Income Tax Return, or IRS Form 1040-NR, also shares similarities with the I-295 form. Form 1040-NR is used by nonresident aliens engaged in business in the U.S. or receiving income from U.S. sources to report their income and deductions. Although focusing more broadly on income tax rather than solely on real estate transactions, like the I-295, it addresses the tax responsibilities of nonresidents, ensuring compliance with U.S. tax laws.

The IRS Form 3520-A, Annual Information Return of Foreign Trust With a U.S. Owner, parallels the I-295 in its focus on reporting and compliance for foreign entities interacting with U.S. assets. While Form 3520-A is specific to trusts, the concept of ensuring foreign entities meet U.S. reporting and tax obligations is a common theme shared with the I-295 affidavit, which deals with nonresident sellers of real estate.

Similar in context to the I-295 is the Statement of Withholding on Dispositions by Foreign Persons of U.S. Real Property Interests, Form 8288-B. This form is an application for a withholding certificate for dispositions by foreign persons of U.S. real property interests, used to determine the amount to be withheld from the disposition proceeds. Both documents serve the overarching purpose of managing and documenting withholding requirements, though they target different aspects of real estate transactions.

Affidavit of Residence forms, used commonly in various legal and school district documentation to verify a person's residential address, share a fundamental focus on residency status with the I-295. While they are used in vastly different situations, both forms require sworn statements regarding the personal circumstances of the individual or entity, underscoring the importance of accuracy and truthfulness in legal affidavits.

The similarities between these documents and the I-295 form underscore the complex web of legal and tax obligations that govern real estate transactions, specifically highlighting the nuance of handling nonresident sellers. Each document, while unique in its application, plays a critical role in ensuring the integrity of real estate reporting, taxation, and regulatory compliance.

Dos and Don'ts

When you are filling out the I-295 form for the State of South Carolina, it's crucial to pay attention to both the details you include and the procedures you follow. Below is a list of key dos and don’ts to assist in completing the form correctly:

- Do read the SC Revenue Ruling #09-13 carefully along with the advisory opinion to fully understand the requirements and implications.

- Do ensure all personal and property-related information is accurate, including the description of the real and tangible personal property being sold.

- Do attach all required documentation, such as a description of the property and any other mandatory attachments specified in the form.

- Do include your correct Social Security Number (SSN) or Federal Employer Identification Number (FEIN), as failing to do so could delay the process.

- Don’t overlook the necessity to report the sale on a timely filed South Carolina income tax return if applicable.

- Don’t leave any sections blank unless they are truly not applicable to your situation. In such cases, indicate with “N/A” or a similar notation.

- Don’t guess on amounts or data points; confirm all information for accuracy before submitting the form.

- Don’t ignore the instructions related to specific situations, such as like-kind exchanges, installment sales, or nonrecognition provisions under IRS codes, as these have specific requirements for reporting and acknowledgment within the form.

Following these guidelines will help ensure the process is completed smoothly and efficiently. Remember, the accuracy and completeness of the form are paramount to comply with South Carolina's tax laws and regulations.

Misconceptions

Understanding forms and legal procedures can often lead to misconceptions, especially when it comes to specific documents like the I-295 form used in the state of South Carolina. Here are seven common misconceptions about the I-295 form and the truths behind them:

The I-295 form is only for individuals. Contrary to this belief, the I-295 form is for both individuals and businesses. It addresses nonresident sellers, which can include corporations and other entities, especially in scenarios where the seller is considered a deemed resident for tax purposes.

Filing the I-295 form relieves the seller of all tax liabilities. While the completion and submission of the I-295 form are part of the process to ensure proper withholding and reporting, it does not automatically relieve the seller of all tax responsibilities. Sellers must still comply with additional tax obligations, including filing a South Carolina income tax return in the year of sale.

There’s no need to report the sale on your income tax if you use the I-295 form. This is incorrect. Even if you complete the I-295 form, you are still required to report the sale on your South Carolina income tax return to ensure all taxes are accurately assessed and paid.

All nonresident sales are subject to the terms of the I-295 form. The I-295 form is specifically designed for situations outlined in SC Revenue Ruling #09-13. Not all nonresident real estate transactions may fall under this ruling, so it's crucial to understand the specifics of your sale.

The I-295 form is complex and requires legal help to complete. While legal or professional advice may be beneficial, especially in complicated transactions, the I-295 form is designed to be completed by the seller. Essential information and straightforward instructions are provided to guide sellers through the process.

Nonresident sellers must always withhold the full gain on the sale. The I-295 form allows for various conditions under which withholding can be limited or adjusted. These include scenarios like installment sales, transactions resulting in no recognizable gain, and even cases where withholding is limited to the net proceeds of the sale.

Completing the I-295 automatically updates the Department of Revenue on the sale. Upon completion, the I-295 form is not directed to the Department of Revenue but retained by the parties involved for their records. The seller’s obligation to report the sale on their income tax return is the formal process for informing the state about the transaction.

Clearing up these misconceptions about the I-295 form helps ensure that sellers are properly informed and can fulfill their obligations without unnecessary confusion or errors.

Key takeaways

- Filing the I-295 form is essential for nonresident sellers involved in a real estate transaction in South Carolina. It serves as an affidavit of facts concerning the sale and the seller’s residency status, which influences the withholding requirements.

- The completion of this form requires detailed information about the property being sold, including a description, the county of location, and tax map number(s), as well as personal information about the seller such as name, address, Social Security Number (SSN), or Federal Employer Identification Number (FEIN).

- There are specific conditions outlined in the form that, if met, can relieve the buyer from the responsibility to withhold income at the time of the sale. These include situations like the seller being a resident or deemed resident of South State Carolina, transactions involving tax-exempt organizations, and special circumstances such as principal residence sales, involuntary conversions, like-kind exchanges, and employee relocations.

- The I-295 form also mandates disclosure of the anticipated gain from the sale and details about how the seller intends to report the sale for income tax purposes. This includes whether the sale will be reported through the installment sale method or if the gain will be reported in its entirety in the year of the sale.

More PDF Templates

South Carolina Controlled Substance License - Submission of the DHEC 3422 form is a step towards compliance with regulations governing asbestos abatement and management.

South Carolina Tax Forms - South Carolina's tax law nuances, like the treatment of net operating losses, are relevant when filing an SC1040X.