Fill Your L Bw 602 Template

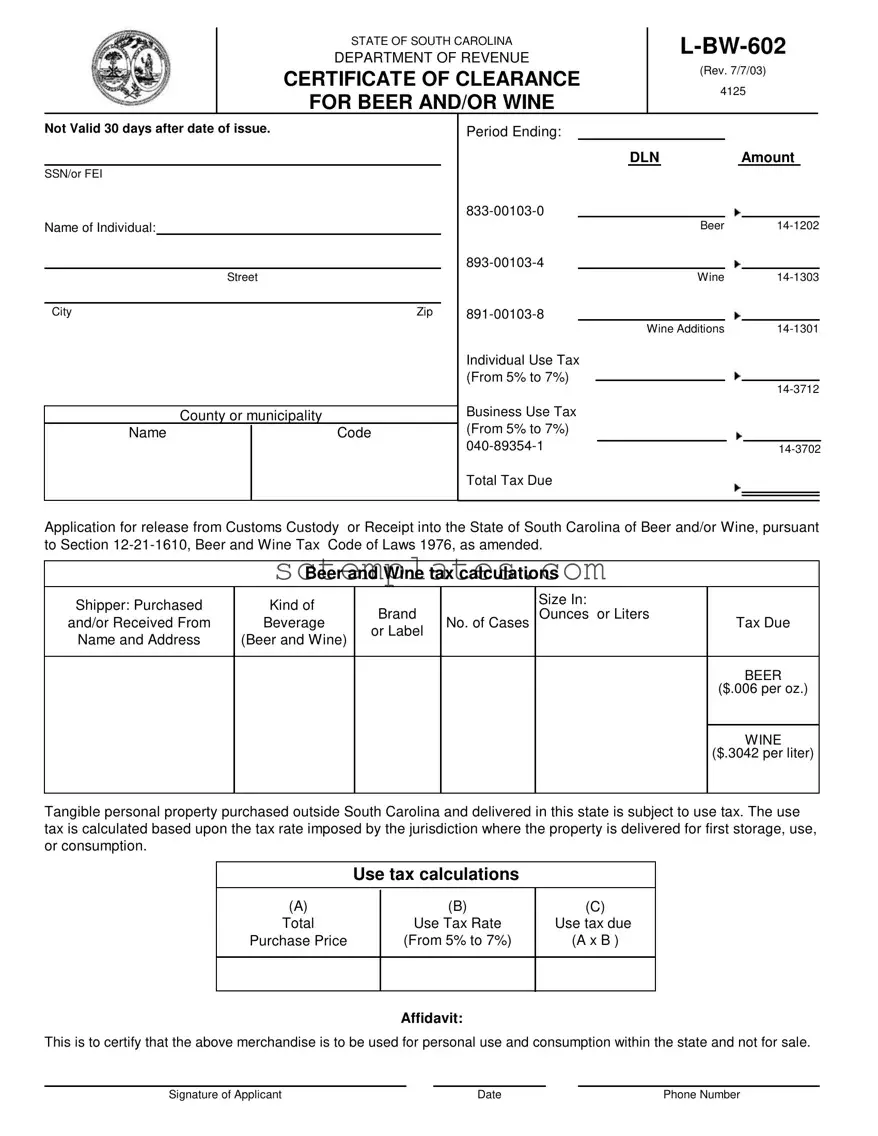

The South Carolina Department of Revenue issues the L-BW-602 form, a crucial document for individuals and businesses engaged in the importation and use of beer and/or wine within the state. Marked by its comprehensive approach to the tax obligations related to beer and wine, this certificate of clearance ensures compliance with Section 12-21-1610 of the Beer and Wine Tax Code of Laws 1976, as amended. Its significance lies in the meticulous calculation of taxes due, incorporating both excise taxes on the quantity purchased and use taxes on tangible personal property brought into South Carolina for personal or business consumption. Not valid after 30 days from the date of issue, the L-BW-602 form facilitates the smooth transaction of alcohol-related business by determining the tax based on the size, quantity, and type of product, thus ensuring that the appropriate excise and use taxes are accurately calculated and paid. This form, which must be completed in triplicate, plays a pivotal role in the regulation of alcohol distribution within the state, underscoring the importance of thorough documentation and compliance with state tax laws. Beyond its immediate function, the form also addresses concerns of privacy under the Social Security Privacy Act and the Family Privacy Protection Act, safeguarding personal information against unauthorized public disclosure and commercial exploitation.

Document Example

|

STATE OF SOUTH CAROLINA |

|

|

DEPARTMENT OF REVENUE |

|

|

(Rev. 7/7/03) |

|

|

CERTIFICATE OF CLEARANCE |

|

|

4125 |

|

|

FOR BEER AND/OR WINE |

|

|

|

Not Valid 30 days after date of issue. |

|

|

Period Ending: |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

DLN |

|

|

Amount |

||||

SSN/or FEI |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of Individual: |

|

|

|

|

|

Beer |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Street |

|

|

|

|

|

Wine |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

Zip |

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

Wine Additions |

|

||||||

|

|

|

|

|

Individual Use Tax |

|

|

|

|

|

|

|

|||

|

|

|

|

|

(From 5% to 7%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

Business Use Tax |

|

|

|

|

|

|

|

|||

|

County or municipality |

|

|

|

|

|

|

|

|

|

|||||

|

|

|

(From 5% to 7%) |

|

|

|

|

|

|

|

|||||

Name |

|

Code |

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

Total Tax Due |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Application for release from Customs Custody or Receipt into the State of South Carolina of Beer and/or Wine, pursuant to Section

Beer and Wine tax calculations

Shipper: Purchased |

Kind of |

|

|

Size In: |

|

Brand |

|

Ounces or Liters |

|

||

and/or Received From |

Beverage |

No. of Cases |

Tax Due |

||

Name and Address |

(Beer and Wine) |

or Label |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

BEER |

|

|

|

|

|

($.006 per oz.) |

|

|

|

|

|

|

|

|

|

|

|

WINE |

|

|

|

|

|

($.3042 per liter) |

|

|

|

|

|

|

Tangible personal property purchased outside South Carolina and delivered in this state is subject to use tax. The use tax is calculated based upon the tax rate imposed by the jurisdiction where the property is delivered for first storage, use, or consumption.

Use tax calculations

(A) |

|

(B) |

(C) |

|

|||

Total |

|

Use Tax Rate |

Use tax due |

Purchase Price |

|

(From 5% to 7%) |

(A x B ) |

|

|

|

|

|

|

|

|

Affidavit:

This is to certify that the above merchandise is to be used for personal use and consumption within the state and not for sale.

Signature of Applicant |

Date |

Phone Number |

Instructions for

Beer or Wine Tax

Enter the total number cases of beer or wine purchased in the column labeled "Number of Cases".

In the column labeled "size in ounces or liters", multiply the total number of cans or bottles per case by the number of ounces or liters per can or bottle to get the total number of ounces or liters purchased per case. Enter this amount in the column labeled "size in ounces or liters".

To get the total number of ounces of beer or liters of wine purchased, multiply the total number of ounces or liters per case by the number of cases. To calculate the tax due, multiply the total number of ounces of beer by $.006 per ounce (beer tax rate) or liters of wine by $.3042 per liter (wine tax rate) purchased.

Use Tax

Purchases of wine, beer and other tangible personal property for use in South Carolina are subject to this state's use tax when no South Carolina sales or use tax has been paid. The State's basic use tax rate is five percent (5%) of the sales price. Some counties impose a local tax in addition to the State's basic rate. To verify a county's tax rate or to determine if a county tax rate is applicable, please call (803)

To calculate the tax due, multiply the total sales price by five percent (5%) (State's basic tax rate) and the sales or use tax rate for the county (currently from 1% to 2%) where the beer or wine will be delivered for storage, use or consumption in this state.

This form must be made in triplicate, original retained by SC Department of Revenue, one copy to be left with Collector of Customs (where applicable) and one copy retained by individual as proof of payment of taxes due.

Social Security Privacy Act Disclosure

It is mandatory that you provide your social security number on this tax form, if you are an individual. 42 U.S.C 405(c)(2)(C)(i) permits a state to use an individual's social security number as means of identification in administration of any tax. SC Regulation

The Family Privacy Protection Act

Under the Family Privacy Protection Act, the collection of personal information from citizens by the Department of Revenue is limited to the information necessary for the Department to fulfill its statutory duties. In most instances, once this information is collected by the Department, it is protected by law from public disclosure. In those situations where public disclosure is not prohibited, the Family Privacy Protection Act prevents such information from being used by third parties for commercial solicitation purposes.

Mail to: |

SC Department of Revenue, License Tax, Columbia SC |

Phone: |

(803) |

|

|

|

FOR OFFICE USE ONLY |

This is to certify that the following taxes: |

|

Beer Excise Taxes in the amount of _________________ and /or Wine Excise Taxes in the amount of ________________ |

|

Use Taxes in the amount of ______________________ |

|

have been paid to the SC Department of Revenue on this __________ day of ________________ , 20 ______ . |

|

Department of Revenue |

Signature and Title |

Form Properties

| Fact | Detail |

|---|