Fill Your Pt 420 Template

Within the intricate labyrinth of state taxation, the PT-420 form emerges as a pivotal piece of documentation for utility and railroad companies operating within the borders of South Carolina. Mandated by the South Carolina Department of Revenue, this form serves as a comprehensive property tax return, necessitating annual submission prior to the strict deadline of April 30 to avoid penalties as prescribed by law. Unpacking the PT-420 form unveils a detailed structure that requires full disclosure of gross investments in each taxing district, a meticulous listing of owned assets including pollution control equipment and licensed vehicles, alongside their respective depreciation schedules. Furthermore, it demands inclusion of annual financial reports submitted to regulatory bodies, a methodological breakdown for determining exempt property, and a precise delineation of construction work in progress. For entities straddling state lines, additional documentation addressing revenue allocations and investments vis-a-vis their South Carolina operations becomes imperative. This thorough and obligatory submission ensures an equitable assessment and taxation process, reinforcing the legal and financial responsibilities of utility and railroad companies in adherence to the 1976 Code of Laws and its subsequent amendments. Embedded within this process is a declaration of accuracy and completeness by the filing parties, underscoring the seriousness with which this form and its contents are considered by both the corporations and the state. The act of navigating and fulfilling the PT-420's exhaustive requirements not only aids in maintaining fiscal compliance but also contributes to the broader economic fabric of South Carolina.

Document Example

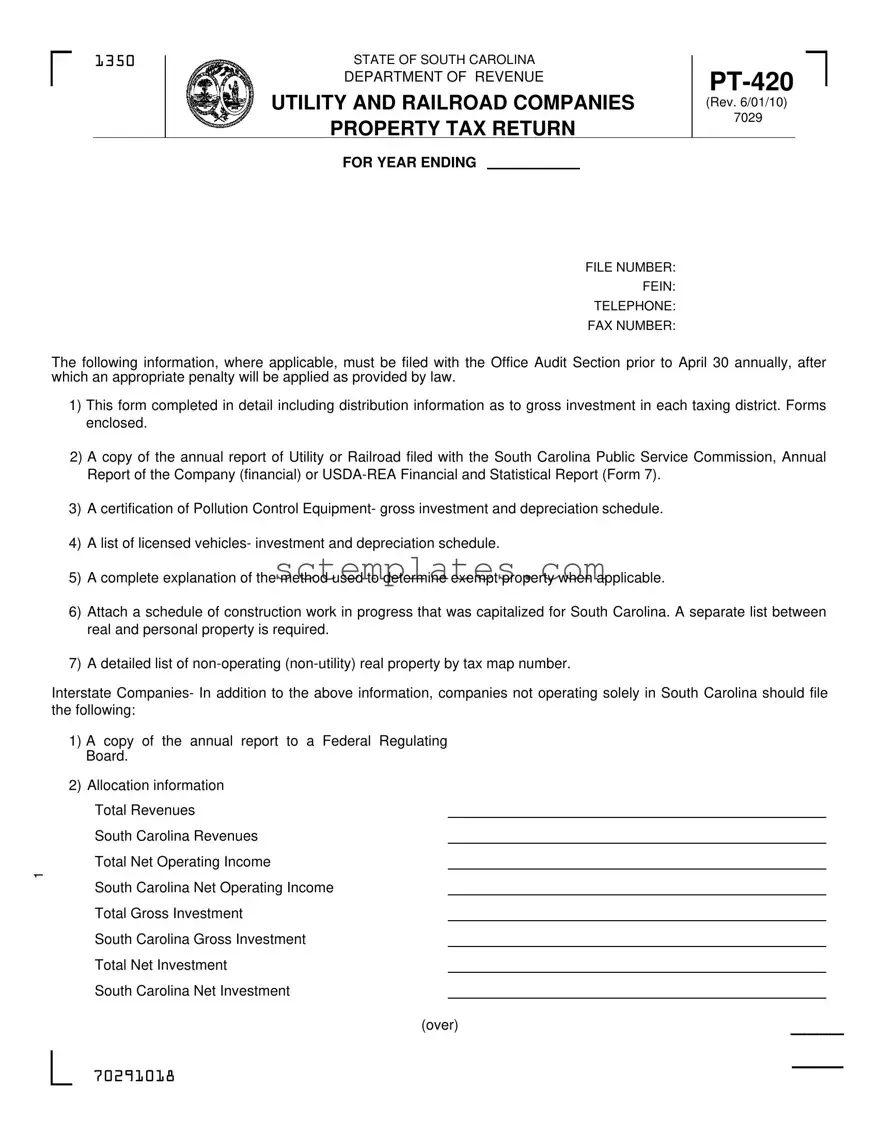

1350

STATE OF SOUTH CAROLINA |

|

|||

DEPARTMENT OF REVENUE |

||||

UTILITY AND RAILROAD COMPANIES |

||||

(Rev. 6/01/10) |

||||

PROPERTY TAX RETURN |

7029 |

|||

|

||||

FOR YEAR ENDING |

|

|

|

|

FILE NUMBER:

FEIN:

TELEPHONE:

FAX NUMBER:

The following information, where applicable, must be filed with the Office Audit Section prior to April 30 annually, after which an appropriate penalty will be applied as provided by law.

1)This form completed in detail including distribution information as to gross investment in each taxing district. Forms enclosed.

2)A copy of the annual report of Utility or Railroad filed with the South Carolina Public Service Commission, Annual Report of the Company (financial) or

3)A certification of Pollution Control Equipment- gross investment and depreciation schedule.

4)A list of licensed vehicles- investment and depreciation schedule.

5)A complete explanation of the method used to determine exempt property when applicable.

6)Attach a schedule of construction work in progress that was capitalized for South Carolina. A separate list between real and personal property is required.

7)A detailed list of

Interstate Companies- In addition to the above information, companies not operating solely in South Carolina should file the following:

1)A copy of the annual report to a Federal Regulating Board.

2)Allocation information

Total Revenues

South Carolina Revenues

Total Net Operating Income

1

South Carolina Net Operating Income

Total Gross Investment

South Carolina Gross Investment

Total Net Investment

South Carolina Net Investment

(over) |

____ |

70291018

I declare that this return including any accompanying schedules and statements has been examined by me and to the best of my knowledge and belief is a true and complete return made in good faith pursuant to the 1976 Code of Laws and amendments.

Taxpayer's Signature |

Title |

Date |

Accountant's Signature |

Title |

Date |

Contact Person |

Tax Preparer / Contact Phone Number |

Returns found incomplete or improper will be returned to the taxpayer for completion or amendment.

Mail completed returns to:

South Carolina Department of Revenue

Utilities

Columbia, SC

70292016

Form Properties

| # | Fact | Governing Law(s) |

|---|---|---|

| 1 | The PT-420 form is specifically designed for utility and railroad companies in South Carolina. | 1976 Code of Laws of South Carolina and amendments. |

| 2 | It must be filed annually with the Office Audit Section by April 30 to avoid penalties. | South Carolina Department of Revenue Regulations. |

| 3 | The form requires detailed information on gross investment distribution in each taxing district. | South Carolina Property Tax Laws. |

| 4 | Submission should include a copy of the annual report filed with the South Carolina Public Service Commission or equivalent, and specific financial and statistical reports. | South Carolina Public Service Commission Regulations. |

| 5 | A certification of Pollution Control Equipment and related schedules must be attached. | Environment and Health Regulations of South Carolina. |

| 6 | Interstate companies are required to include additional information such as a copy of the annual report to a Federal Regulating Board and allocation information. | Interstate Commerce Commission Regulations. |

| 7 | The form necessitates a declarative statement by the submitting party affirming the completeness and accuracy of the information provided. | 1976 Code of Laws of South Carolina, truth-in-taxation provisions. |

Guide to Writing Pt 420

Preparing the PT-420 form is crucial for Utility and Railroad Companies operating within South Carolina, ensuring compliance with state tax obligations. The form helps these entities to accurately report their property taxes within the stipulated deadline to avoid penalties. It is essential to provide detailed and accurate information to reflect the company's financial and operational status for the year ending. Below are step-by-step instructions to successfully fill out and submit the PT-420 form.

- Begin by gathering all required documents and information, including the company’s annual financial report, a list of licensed vehicles, and detailed investment and depreciation schedules.

- Enter the company's FILE NUMBER, FEIN, TELEPHONE, and FAX NUMBER in the designated fields at the top of the form.

- Complete the form in detail, ensuring to include distribution information regarding the gross investment in each taxing district. Attach the forms mentioned as enclosed.

- Attach a copy of the annual report filed with the South Carolina Public Service Commission or the corresponding financial report for Utility or Railroad companies, including the USDA-REA Financial and Statistical Report (Form 7) if applicable.

- Include a certification of Pollution Control Equipment, listing both the gross investment and the depreciation schedule.

- Provide a list of licensed vehicles along with their investment and depreciation schedule.

- Explain the method used to determine exempt property, if applicable.

- Attach a schedule detailing construction work in progress that has been capitalized for South Carolina. Ensure to differentiate between real and personal property.

- Create a detailed list of non-operating (non-utility) real property, identifying each by tax map number.

- For interstate companies, add a copy of the annual report to a Federal Regulating Board and provide allocation information such as Total Revenues, South Carolina Revenues, Total Net Operating Income, South Carolina Net Operating Income, Total Gross Investment, and South Carolina Gross Investment.

- Review the form and attached documents for accuracy. Then, complete the declaration section by signing and dating the form. Ensure that both the taxpayer and the accountant sign and title the form appropriately.

- Include the contact information for the person or tax preparer responsible for the form, ensuring a phone number is provided for any queries or clarifications.

- Mail the completed form and all attachments to South Carolina Department of Revenue Utilities, Columbia, SC 29214-0306 before the deadline to avoid penalties.

By following these steps carefully, Utility and Railroad Companies can ensure compliance with South Carolina's tax laws, avoiding delays and penalties associated with late or inaccurate filings. Remember, it's crucial to provide complete and accurate information to reflect your company's operations throughout the fiscal year.

Understanding Pt 420

What is the PT-420 form?

The PT-420 form is a document specifically designed for utility and railroad companies to file their property tax returns in the State of South Carolina. The form requires detailed information to be submitted annually to the Office Audit Section of the Department of Revenue, including gross investment distribution across taxing districts, financial reports, and other pertinent information related to the company's operations and property within the state.

When is the due date for filing the PT-420 form?

Utility and railroad companies must ensure that their PT-420 form is filed with the South Carolina Department of Revenue prior to April 30 each year. Submissions after this date are subject to penalties as stipulated by law.

What information must be included with the PT-420 form?

Companies need to provide a comprehensive package including the PT-420 form filled out in detail, a copy of the company’s annual report filed either with the South Carolina Public Service Commission or another relevant body, certification of pollution control equipment, investment and depreciation schedules for licensed vehicles, explanations of exempt property, schedules for construction work in progress, and a detailed list of non-operating real property. For companies not solely operating in South Carolina, additional reports to a federal regulating board and allocation information are required.

What happens if the PT-420 form is submitted late or incomplete?

If the PT-420 form is submitted after the April 30 deadline, or if the submission is found to be incomplete, the South Carolina Department of Revenue will impose penalties according to state law. Incomplete returns will be returned to the taxpayer for completion or amendment, further delaying the processing and potentially incurring additional penalties.

Who needs to sign the PT-420 form?

The PT-420 form must be signed by an authorized taxpayer within the submitting utility or railroad company, affirming the accuracy and completeness of the information provided. An accountant or another authorized individual should co-sign the document, alongside providing their respective titles and the contact details of a person who can be reached for further queries.

Where should the completed PT-420 form be sent?

Once filled out and signed, the completed PT-420 form, along with all required documentation and schedules, should be mailed to the South Carolina Department of Revenue’s office dedicated to utilities, with the specific address being: South Carolina Department of Revenue Utilities, Columbia, SC 29214-0306. It’s recommended to ensure the package is complete to avoid the need for resubmission.

Common mistakes

Failing to complete the PT-420 form in detail, especially disregarding the requirement to provide distribution information regarding the gross investment in each taxing district, is a common mistake. This overlook can result in an incomplete submission, leading to a request for amendment, delaying the processing time.

Not attaching a copy of the annual report filed with the South Carolina Public Service Commission, or, for certain entities, the USDA-REA Financial and Statistical Report (Form 7). This documentation is critical for verifying the financial information reported on the PT-420 form.

Omitting the certification of Pollution Control Equipment, including both the gross investment and depreciation schedule, might lead to inaccuracies in determining the taxable assets of the company.

Another frequent error is neglecting to list licensed vehicles alongside their investment and depreciation schedule. Such an omission provides an incomplete picture of the company's taxable personal property.

Incorrectly explaining or entirely neglecting to detail the method used to determine exempt property. This detail is essential for identifying property that should not be taxed, and any mistake here can lead to incorrect tax assessments.

Forgetting to attach a schedule of construction work in progress that was capitalized for South Carolina, separately listing real and personal property. This specific detail is crucial for determining the accurate tax due, as it influences the amount of capital investment to be taxed.

Additionally, companies operating inter-state often make the mistake of not providing:

A copy of the annual report to a Federal Regulating Board. This oversight can affect the accurate allocation of revenue and investment between South Carolina and other states, potentially resulting in erroneous tax calculations.

Proper allocation information including total revenues and net operating income, both within South Carolina and overall. This mistake can lead to inaccurate assessments of taxes owed, as it directly affects the determination of the company's operating presence and profitability within the state.

Each of these errors can delay the processing of the PT-420 form, lead to the necessity of amendments, and potentially result in penalties as outlined by law. It's essential for utility and railroad companies to carefully review all requirements and ensure that each section of the PT-420 form is completed accurately and in its entirety.

Documents used along the form

When businesses engage with the PT-420 form for the State of South Carlson Department of Revenue, focusing on utilities and railroad companies property tax return, they navigate through a structured pathway of compliance. To fully comply and make the most out of their submission, there exists a suite of essential documents and forms that often accompany the PT-420. Each of these documents serves a unique purpose, streamlining the process to ensure accuracy and meet regulatory requirements.

- Annual Report to the South Carolina Public Service Commission: This report provides a comprehensive overview of the company's operational, financial, and service delivery performance over the fiscal year. It is critical for demonstrating compliance with state regulations and standards for utility and railroad operations.

- USDA-REA Financial and Statistical Report (Form 7): Essential for companies operating under the United States Department of Agriculture Rural Electrification Administration, this report outlines the financial health and operational statistics of the company, offering insights into fiscal management and efficiency.

- Certification of Pollution Control Equipment: A document certifying the gross investment and depreciation schedule of equipment used for pollution control. It highlights the company's commitment to environmental stewardship and adherence to regulations governing pollution.

- List of Licensed Vehicles: This includes investment and depreciation schedules for all licensed vehicles owned by the utility or railroad company. It helps in calculating personal property taxes applicable to these assets.

- Construction Work in Progress Schedule: A document detailing any construction projects that were capitalized in South Carolina, separated into categories of real and personal property. It aids in understanding the tax implications of ongoing construction investments.

- List of Non-operating Real Property: Provides detailed information on non-operational or non-utility real property owned by the company, identified by tax map number. It's crucial for accurate real estate property tax assessments.

- Annual Report to a Federal Regulating Board: For companies not solely operating within South Carolina, this report to the relevant federal board outlines the company’s broader performance and compliance with federal regulations, complementing state-level reporting.

Together, these documents form a mosaic of compliance, each piece integral to the complete picture required by the South Carolina Department of Revenue. They ensure that utility and railroad companies not only meet their tax obligations but also maintain transparency and accountability in their operations. The thoughtful completion and submission of these documents, alongside the PT-420 form, pave the way for a smooth tax return process.

Similar forms

The PT-420 Utility and Railroad Companies Property Tax Return shares characteristics with the Schedule C (Profit or Loss from Business) used in U.S. federal tax filing. Just like the PT-420 form requires detailed distribution information and gross investment by tax district, Schedule C necessitates a breakdown of income and expenses related to a sole proprietor's business activities. Both forms serve as tools for reporting financial operations to a governing tax authority, albeit on different scales and for different jurisdictions, but ultimately aim to assess tax based on reported financial activity.

Similarly, the PT-420 form has parallels with the Form 4562 (Depreciation and Amortization) that is used for reporting depreciation on assets in federal tax returns. The requirement on the PT-420 to provide a certification of Pollution Control Equipment including a gross investment and depreciation schedule aligns with the purpose of Form 4562. Both documents require detailed listings and calculations of depreciation, offering a structured way to report how assets decrease in value over time, which affects the overall tax obligations of the entity.

The requirement to attach annual reports filed with the South Carolina Public Service Commission or the USDA-REA Financial and Statistical Report (Form 7) resembles the SEC Form 10-K filing requirement for publicly traded companies. The 10-K offers a comprehensive overview of the company's financial condition and is filed annually with the Securities and Exchange Commission. Both the PT-420's and the 10-K's disclosure of financial information provide transparency and a basis for taxation or investment decisions, underscoring the importance of financial accountability in both the corporate and tax realms.

PT-420's stipulation for a complete explanation of the method used to determine exempt property mirrors the function of Form 8949 (Sales and Other Dispositions of Capital Assets) in federal taxes, where taxpayers must detail the sale or exchange of capital assets not reported on another form. Although serving different purposes—one for tax exemption substantiation and the other for capital gains or losses reporting—both forms require precise documentation about specific assets to ensure accurate tax treatment.

The request on the PT-420 form for a schedule of construction work in progress that was capitalized touches on the realm of Form 3115 (Application for Change in Accounting Method). When a business decides to capitalize construction work in progress, it might need to change its accounting method for tax purposes. Like the PT-420's interest in how such work affects taxation within South Carolina, Form 3115 addresses the broader IRS regulations governing how changes to accounting methods impact tax liabilities.

Moreover, the requirement to attach a detailed list of non-operating (non-utility) real property by tax map number on the PT-420 form echoes the informational needs of the Form 8825 (Rental Real Estate Income and Expenses of a Partnership or an S Corporation). Both require detailed disclosures about real estate, although for different administrative reasons. While PT-420 focuses on tax implications within a specific state context, Form 8825 provides the federal government with data on how real estate activities impact tax obligations for entities with special tax statuses.

Lastly, the PT-420's need for interstate companies to file allocation information and annual reports to a Federal Regulating Board is reminiscent of the Multi-State Corporation Income Tax Return practices. These practices require corporations operating in multiple states to allocate and apportion income based on business activity within each state. This ensures that each state receives its fair share of tax revenue from the corporation's total income, analogous to how the PT-420 aims to ensure South Carolina collects appropriate taxes based on in-state business activities.

Dos and Don'ts

When it comes to completing the PT-420 form for Utility and Railroad Companies Property Tax Return in South Carolina, precision, accuracy, and timeliness are key. Ensuring your form is meticulously filled can avert unnecessary penalties and facilitate a smoother audit process. Here are five essential dos and don'ts that can guide you through this crucial endeavor:

Do:- Review all requirements thoroughly before beginning. Familiarize yourself with every section to make sure you understand what information is needed. This preparatory step cannot be overstated.

- Provide detailed and accurate information for each part of the form, including distribution information related to the gross investment in each taxing district and all supplementary documents as listed.

- Ensure that all documents are complete and up to date, including a copy of the annual report filed with the South Carolina Public Service Commission or the equivalent, the certification of Pollution Control Equipment, and any other required schedules and reports.

- Verify the method used to determine the exempt property is clearly explained and accurately reflected in your submission, as this will be a focal point during the review process.

- Sign and date the form with the appropriate signatures. Remember, the declaration asserts that to the best of your knowledge, the return is truthful and complete. This attestation is not to be taken lightly.

- Procrastinate. Waiting until the last moment can lead to errors and omissions. The deadline of April 30 is firm, and penalties for late submission are imposed as mandated by law.

- Overlook sections that may seem irrelevant. If a section does not apply, noting it as ‘Not Applicable’ is preferable to leaving it blank, which might raise questions about the completeness of your return.

- Fill out the form by hand if your handwriting is difficult to read. A typed document ensures clarity and reduces the risk of misinterpretation or data entry errors by the Department of Revenue.

- Ignore the requirement for specific lists, such as the detailed list of non-operating (non-utility) real property by tax map number, and the segmentation between real and personal property. These lists are crucial for accurate tax assessment.

- Submit your return without double-checking every section for completeness and accuracy. An oversight can result in your return being sent back for amendment, delaying the process unnecessarily.

Filling out the PT-420 form with diligence and attention to detail is not merely about compliance; it is an integral part of fiscal responsibility for utility and railroad companies operating in South Carolina. By adhering to these dos and don'ts, companies can ensure they represent their property, investments, and income accurately and avoid penalties or audits that could arise from inaccuracies or incomplete information.

Misconceptions

The Pt 420 form, required by the State of South Carolina Department of Revenue, is a specialized document designed for utility and railroad companies to file their property tax returns. Misunderstandings surrounding this form can lead to errors in compliance, potentially resulting in fines or penalties for the companies involved. Here, we aim to clarify some of the common misconceptions associated with the Pt 420 form.

- Misconception #1: The Pt 420 form is required for all businesses operating within South Carolina.

This is incorrect. The Pt 420 form is specifically designed for utility and railroad companies. Other types of businesses must use different forms tailored to their specific reporting requirements set forth by the South Carolina Department of Revenue.

- Misconception #2: The form can be filed at any time during the year.

Actually, there is a strict deadline for filing the Pt 420 form. It must be submitted to the Office Audit Section prior to April 30 annually. Failure to meet this deadline may result in penalties as outlined by South Carolina law.

- Misconception #3: The Pt 420 form is a simple declaration of earnings.

Contrary to this belief, the Pt 420 form requires detailed information beyond just earnings. This includes distribution information related to gross investment in each taxing district, a copy of the annual report filed with the South Carolina Public Service Commission, and specific schedules detailing investment, depreciation, and construction work in progress, among others. Its comprehensive nature ensures a thorough assessment of the tax obligations of utility and railroad companies.

- Misconception #4: Online submission of the Pt 420 form is available to all companies.

As of the latest available information, the form must be mailed to the South Carolina Department of Revenue's specified address. There is no indication that electronic submission is universally accepted for this particular form, underscoring the importance of planning to meet the annual filing deadline.

- Misconception #5: If a company operates in multiple states, only the information for South Carolina needs to be filled out.

This statement does not fully capture the reporting requirements. While the primary focus of the Pt 420 form is indeed on the company's activities within South Carolina, interstate companies are also required to submit additional documentation. This includes a copy of the annual report to a Federal Regulating Board and allocation information comparing South Carolina revenues and investments to overall figures. This ensures accurate taxation reflective of the company's operations within the state vis-à-vis its overall operations.

In conclusion, navigating the complexities of the Pt 420 form demands attention to specific details and deadlines. Misconceptions can lead to unintentional non-compliance, emphasizing the importance of a thorough understanding of the form’s requirements. Utility and railroad companies must exercise due diligence in gathering the necessary information and adhering to South Carolina’s regulatory framework to ensure accurate and timely submissions.

Key takeaways

Filling out and submitting the PT-420 form is a crucial annual task for utility and railroad companies operating in South Carolina. Understanding the requirements and deadlines can help avoid penalties and ensure compliance with state tax regulations. Here are key takeaways:

- Companies must submit the PT-420 form to the South Carolina Department of Revenue by April 30 each year. Late submissions are subject to penalties as dictated by state law.

- The form requires detailed financial information, including gross investment distribution across different taxing districts. This ensures accurate tax assessment based on the location of assets.

- In addition to the PT-420 form, companies must provide a copy of their annual report to the South Carolina Public Service Commission or an equivalent financial report. This confirms the financial health and operational status of the company.

- A comprehensive list and valuation of pollution control equipment, as well as licensed vehicles, must be included. This includes both the initial investment and the depreciation schedule, affecting the taxable value of these assets.

- Companies must also outline the methodology used to determine exempt property. This helps the Department of Revenue understand the basis for any exemptions claimed on the tax return.

- For construction work in progress that was capitalized specific to South Carolina, a separate schedule distinguishing between real and personal property is necessary.

- Interstate companies are required to submit additional documentation, including an annual report to a federal regulating board and detailed allocation information to accurately apportion their South Carolina tax liability based on operational revenues and investments.

Overall, careful attention to the details and requirements of the PT-420 form is essential for utility and railroad companies to remain compliant with South Carolina's tax regulations. Ensuring all required documents and information are accurately compiled and submitted by the deadline can prevent unnecessary penalties and contribute to a smooth tax filing process.

More PDF Templates

Dhec 4024 Form Printable - By centralizing certification requirements, the DHEC 2351 form simplifies the application process for candidates.

Immigration Bond Refund - The I-312 form is a critical document for nonresidents to understand and utilize when engaging in temporally based services in South Carolina.