Fill Your Sc 1120 T Template

Filing taxes and managing extensions is an integral part of corporate operations, especially in South Carolina where the SC1120-T form plays a crucial role. Tailored for businesses that anticipate owing income tax or license fees, this form serves as both a tentative corporation tax return and a request for a conditional extension. Due originally when tax returns are filed, the SC1120-T ensures companies meet their obligations by allowing them to submit a tentative tax owed, thus avoiding penalties for not paying at least ninety percent of their total due tax by the deadline. For those expecting no dues and holding a federal extension, South Carolina offers leniency by accepting federal documentation, provided corporate returns are submitted within the IRS's extended timeframe. Moreover, this form outlines specific guidelines for consolidated return filers, underscoring the importance of listing all corporates involved to maintain the option for a consolidated return, with instructions on calculating license fees for each listed entity. It’s also noted that savings and loan associations or banks are exempt from the license fee. Detailed instructions, including the necessity of black ink and including pertinent business information with submitted payments, streamline the process, ensuring clear communication and compliance with the South Carolina Department of Revenue's requirements.

Document Example

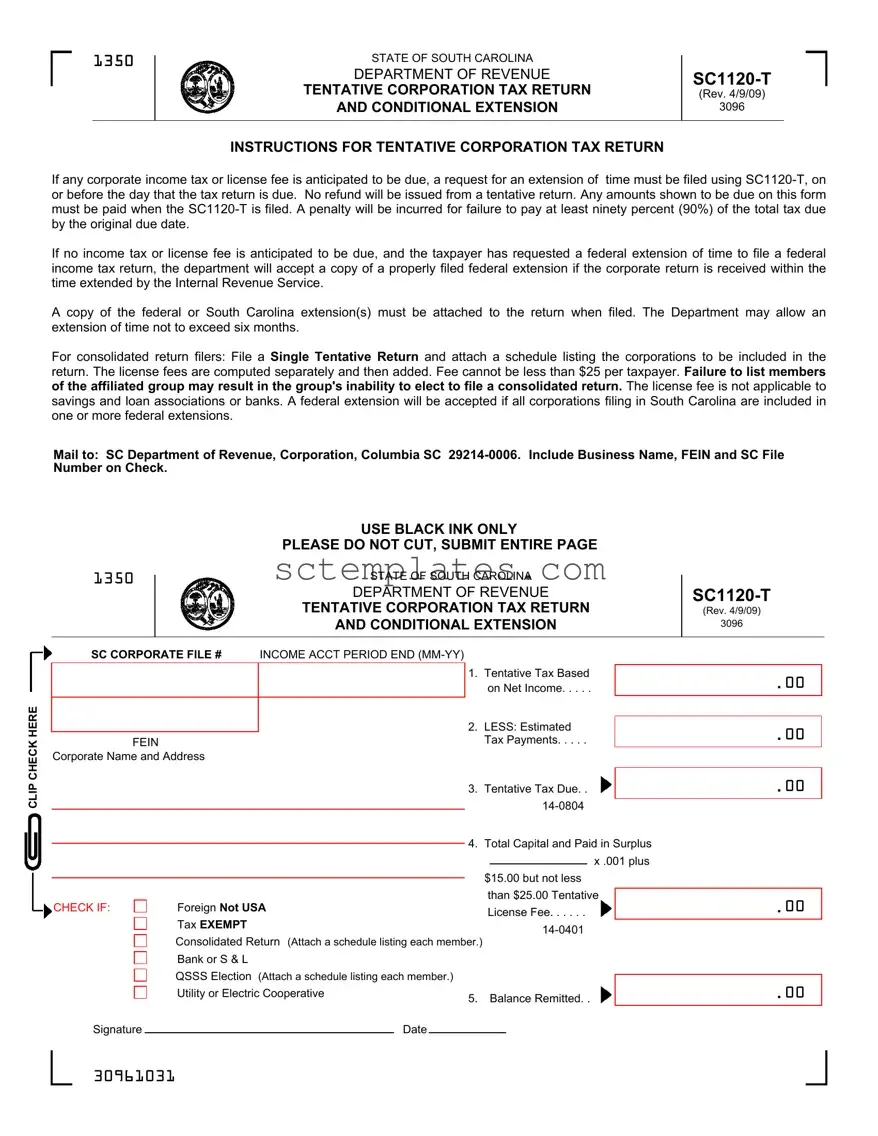

1350

STATE OF SOUTH CAROLINA |

|

|

|

||

DEPARTMENT OF REVENUE |

||

TENTATIVE CORPORATION TAX RETURN |

||

(Rev. 4/9/09) |

||

AND CONDITIONAL EXTENSION |

3096 |

|

|

|

INSTRUCTIONS FOR TENTATIVE CORPORATION TAX RETURN

If any corporate income tax or license fee is anticipated to be due, a request for an extension of time must be filed using

If no income tax or license fee is anticipated to be due, and the taxpayer has requested a federal extension of time to file a federal income tax return, the department will accept a copy of a properly filed federal extension if the corporate return is received within the time extended by the Internal Revenue Service.

A copy of the federal or South Carolina extension(s) must be attached to the return when filed. The Department may allow an extension of time not to exceed six months.

For consolidated return filers: File a Single Tentative Return and attach a schedule listing the corporations to be included in the return. The license fees are computed separately and then added. Fee cannot be less than $25 per taxpayer. Failure to list members of the affiliated group may result in the group's inability to elect to file a consolidated return. The license fee is not applicable to savings and loan associations or banks. A federal extension will be accepted if all corporations filing in South Carolina are included in one or more federal extensions.

Mail to: SC Department of Revenue, Corporation, Columbia SC

CLIP CHECK HERE

USE BLACK INK ONLY

PLEASE DO NOT CUT, SUBMIT ENTIRE PAGE

1350 |

|

|

STATE OF SOUTH CAROLINA |

|

|

|

||||

|

|

|

|

|||||||

|

|

|

DEPARTMENT OF REVENUE |

|

|

|||||

|

|

|

TENTATIVE CORPORATION TAX RETURN |

(Rev. 4/9/09) |

|

|

||||

|

|

|

AND CONDITIONAL EXTENSION |

3096 |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

SC CORPORATE FILE # |

INCOME ACCT PERIOD END |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

Tentative Tax Based |

|

|

. |

00 |

|

|

|

|

|

|

on Net Income |

|

|

|

||

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

LESS: Estimated |

|

|

|

|

|

|

|

|

|

|

|

. 00 |

|

||||

FEIN |

|

|

Tax Payments |

|

|

|

||||

|

|

|

|

|

|

|

||||

Corporate Name and Address |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||

|

|

|

3. |

Tentative Tax Due. . |

|

. 00 |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CHECK IF:

CHECK IF:

Signature

4. Total Capital and Paid in Surplus x .001 plus

$15.00 but not less than $25.00 Tentative

Foreign Not USA |

License Fee |

||

|

|

||

Tax EXEMPT |

|||

|

|

||

Consolidated Return (Attach a schedule listing each member.) |

|||

Bank or S & L |

|

|

|

QSSS Election (Attach a schedule listing each member.) |

|

|

|

Utility or Electric Cooperative |

5. Balance Remitted. . |

||

|

|

||

Date |

|

|

|

|

|

|

|

.00

.00

30961031

Form Properties

| Fact | Detail |

|---|---|

| Form Purpose | The SC1120-T form is used for filing a tentative corporation tax return and requesting a conditional extension in South Carolina. |

| Due Date | The form must be filed on or before the original due date of the corporate income tax return. |

| Payment Requirement | Any anticipated tax or license fee due must be paid upon filing the SC1120-T form. |

| Penalty for Underpayment | A penalty is imposed for failing to pay at least ninety percent (90%) of the total tax due by the original deadline. |

| Extension Length | The Department of Revenue may grant an extension of time to file, not to exceed six months. |

| Governing Law | The form is governed by South Carolina tax law as administered by the South Carolina Department of Revenue. |

Guide to Writing Sc 1120 T

Filing a SC1120-T, also known as the Tentative Corporation Tax Return, is a crucial step for corporations in South Carolina that anticipate owing income tax or license fees. This process ensures compliance with state tax obligations and helps avoid penalties. Steps outlined here will guide through the completion of this form, supporting a smooth and accurate submission. It's important to pay special attention to the deadline: this form must be filed on or before the due tax return date to potentially secure an extension and to avoid late fees for underpayment. Here's how to do it:

- Start by gathering the necessary information, including the corporation's Federal Employer Identification Number (FEIN), South Carolina Corporate File Number, and the income account period end date (MM-YY).

- Using black ink, enter the corporation's name and address in the designated area at the top of the form.

- In the box labeled "SC Corporate File #," input your South Carolina Corporate File Number.

- Next to "Income Acct Period End (MM-YY)," fill in the end date of the income account period for which you are filing.

- Under "1. Tentative Tax Based on Net Income," enter the tentative tax amount you’ve calculated based on the corporation's net income.

- If any estimated tax payments have already been made, list these under "2. LESS: Estimated Tax Payments" to find out the tentative tax due.

- Determine the "3. Tentative Tax Due" by subtracting your estimated tax payments (if any) from the tentative tax based on net income.

- For the "4. Total Capital and Paid in Surplus" section, calculate the fee by multiplying the total capital and paid-in surplus by .001, adding $15.00 to this amount but ensuring it's not less than $25.00. Enter this fee in the space provided.

- If applicable, mark the checkboxes for "Tentative Foreign Tax EXEMPT," "Consolidated Return," "Bank or S & L," "QSSS Election," or "Utility or Electric Cooperative," and attach any required schedules listing each member as directed.

- Calculate the "5. Balance Remitted" by subtracting any payments already made from the tentative tax due and license fee, then enter this amount.

- Sign and date the form in the designated section at the bottom.

- Finally, attach a check for the balance remitted if applicable, make sure to include the Business Name, FEIN, and SC File Number on the check, and mail the entire page to SC Department of Revenue, Corporation, Columbia, SC 29214-0006.

It’s essential to use black ink throughout and to submit all documents timely to ensure full compliance and to avoid any potential penalties. Filing the SC1120-T form diligently is the first step towards a successful extension request, ensuring that all corporate tax obligations are met appropriately.

Understanding Sc 1120 T

What is the SC1120-T form used for?

The SC1120-T form is utilized for filing a tentative corporation tax return and requesting a conditional extension of time to file the corporate income tax or license fee in South Carolina. This form must be filed by corporations anticipating owing tax or license fees, to avoid penalties. Submitting this form on or before the original tax return due date allows corporations a grace period to prepare and submit the full return without immediate full tax payment.

Who needs to file the SC1120-T form?

Any corporation that anticipates owing corporate income tax or a license fee to the State of South Carolina must file the SC1120-T form. This requirement is also applicable to entities that have filed for a federal extension and owe taxes. Corporations not expecting to owe taxes but have requested a federal extension must attach a copy of the federal extension to their corporate return if filed within the extended period.

Can a corporation request an extension without anticipating any income tax or license fee due?

Yes, a corporation can request an extension without anticipating any income tax or license fee due if it has also requested a federal extension to file its federal income tax return. In such cases, the South Carolina Department of Revenue will accept the federal extension, provided the corporate return is filed within the time frame extended by the Internal Revenue Service.

How is the license fee calculated and what is the minimum payable amount?

The license fee is calculated based on the total capital and paid-in surplus of the corporation, at a rate specified in the form, with a minimum payable amount of $25 per taxpayer. This computation is done separately for each corporation and then added together for those filing a consolidated return. It is important to note that banks and savings and loan associations are not subject to this license fee.

What penalties apply if the tentative tax is not paid by the original due date?

Failure to pay at least ninety percent (90%) of the total tax due by the original due date will result in a penalty. This emphasizes the importance of filing the SC1120-T form and making the necessary tentative tax payment within the required timeframe to avoid penalties.

Common mistakes

When it comes to filling out the SC 1120-T Tentative Corporation Tax Return form for the State of South Carolina, there are several common mistakes that can lead to issues with the Department of Revenue. Avoiding these errors can save significant time and reduce potential fines. Here are nine common pitfalls to be aware of:

Not filing on time: Missing the due date for filing the SC1120-T can result in penalties. It’s crucial to submit the form on or before the original due date, especially if taxes or license fees are anticipated.

Incorrect calculation of taxes due: Overlooking the accurate calculation of tentative tax based on net income leads to either underpayment or overpayment, both of which can create complications.

Failing to pay at least 90% of the total tax due: This specific requirement, if not met, incurs a penalty. Ensuring that at least 90% of the tax due is paid by the original due date is essential.

Omitting FEIN, corporate name, or address: These crucial details identify the taxpayer and their obligation; omitting them may cause your return to process incorrectly.

Incorrect calculation of license fee: For those subject to the license fee, miscalculating it (especially not adhering to the minimum fee per taxpayer) can lead to underpayments and potential issues with the Department of Revenue.

Forgetting to attach a schedule for consolidated returns: When filing a consolidated return, failing to attach a list of all corporations included may jeopardize the ability to file this way.

Failure to attach a copy of the federal extension: If relying on a federal extension and no tax or license fee is due, not attaching a copy of the federal extension can result in non-acceptance of the SC1120-T by the deadline.

Using incorrect ink: The form specifies to use black ink only. Using other colors may result in processing delays or the form being unreadable when scanned.

Not including the required check information: When paying any amounts due, not including the business name, FEIN, and SC File Number on the check can lead to misapplied payments.

Being mindful of these common errors can smooth the process of submitting the SC1120-T form, ensuring compliance with South Carolina’s tax obligations and avoiding unnecessary penalties.

Documents used along the form

Filing the SC1120-T form, known as the Tentative Corporation Tax Return and Conditional Extension, is a critical step for corporations operating in South Carolina seeking an extension on their tax returns. This form, utilized to estimate the tax owed and to request additional time for filing the complete return, often accompanies several other forms and documents to ensure compliance with state regulations. Understanding the relationship and the purpose of these documents is essential for a comprehensive approach to corporate tax filing.

- SC1120: The SC1120, or the South Carolina Corporation Income Tax Return, is a crucial document that corporations must file annually. It details the income, deductions, and credits of the corporation, serving as the final declaration of income tax liability for the year.

- SC1120S: This form is specifically for S corporations operating within South Carolina. The SC1120S details the income, losses, deductions, and credits of the corporation, passing the income through to the shareholders to be reported on their individual income tax returns.

- SC2220: South Carolina Underpayment of Estimated Tax by Corporations, the SC2220, is used when a corporation has not paid enough in estimated tax payments throughout the tax year. This form helps calculate the amount of underpayment and any penalties due.

- SC2848: The Power of Attorney and Declaration of Representative form, SC2848, authorizes an individual, such as an accountant or attorney, to represent the corporation before the Department of Revenue and to receive confidential tax information.

- SC8736: Request for Extension of Time to File South Carolina Returns, SC8736, is applied for extensions beyond the initial extension granted by the SC1120-T. It is essential for corporations that need more time to gather information necessary for their final tax return.

Together, these forms and documents play integral roles in the tax filing process for corporations in South Carolina. They ensure compliance with tax obligations, facilitate proper representation, and manage tax liabilities effectively. It's crucial for corporations to be familiar with these documents, understand their purposes, and file them accurately and timely to avoid penalties and ensure smooth operations.

Similar forms

The Form 1040-ES, used by individuals to calculate and pay estimated quarterly taxes, mirrors the SC1120-T's functionality for corporations, focusing on taxes anticipated to be due within the current tax year. Both forms serve as tools for taxpayers to comply with the pay-as-you-go tax system of the United States, helping avoid underpayment penalties by estimating the tax liability ahead of the final tax return submission.

Form 7004, Request for Automatic Extension of Time to File Certain Business Income Tax, Information, and Other Returns, shares a fundamental goal with the SC1122-T: providing taxpayers more time to file their tax returns. However, Form 7004 is applicable to a broader range of entities, including corporations, partnerships, and certain trusts, offering a parallel at the federal level to the conditional extension mechanism of the SC1120-T.

The SC1040, South Carolina Individual Income Tax Return, although tailored for individual filers rather than corporations, engages with similar principles of tax computation and payment on income. Just as the SC1120-T considers corporate income tax and license fees, the SC1040 assesses income tax due from individuals, reflecting the scale of taxation from individual to corporate entities within South Carolina's tax system.

Another parallel document is the UBT-ES, Estimated Unincorporated Business Tax Payment Voucher for New York City. This form is designed for businesses, rather than corporations, to pay their estimated taxes quarterly. Like the SC1120-T, it underscores the requirement across jurisdictions for business entities to report and pay taxes in advance based on estimated earnings.

The Form 1120, U.S. Corporation Income Tax Return, operates on a national scale, similar to the SC1120-T's state-level function, requiring corporations to report their income, gains, losses, deductions, and credits to the Internal Revenue Service (IRS). Both forms determine the corporation's tax liability, although the SC1120-T is distinct in its tentative nature and its specific application to South Carolina entities.

Form 8832, Entity Classification Election, while not a tax return, influences tax obligations by allowing an entity to choose how it will be taxed (as a corporation, partnership, or disregarded entity). This choice directly affects the filing requirements, including whether an entity must file the SC1120-T, showcasing the interconnectedness of entity classification and tax liability.

The TXP-01, or Texas Franchise Tax Preliminary Report, is similarly used by businesses in Texas to provide a preliminary assessment of their due franchise tax. Like the SC1120-T, it caters to the need for businesses to comply with local tax obligations on a provisional basis, emphasizing the widespread practice of estimated tax payments across states.

The Form 1065, U.S. Return of Partnership Income, while designed for partnerships, encounters parallel grounds with the SC1120-T in the context of reporting income and deductions to calculate tax liability. Although it caters to a different type of entity, the necessity to report and potentially pay estimated tax aligns with the essence of preliminary tax compliance seen in the SC1120-T.

Form 945, Annual Return of Withheld Federal Income Tax, addresses the reporting of non-payroll income tax withheld, incorporating a sense of preemptive financial accountability similar to that of the SC1120-T. Both forms play a crucial role in the respective realms of income and corporate taxation by ensuring proper tax collection and reporting ahead of annual returns.

Lastly, the California Form 100-ES, Corporation Estimated Tax, directly parallels the SC1120-T, as both are designed for corporations to estimate and pay taxes ahead of filing their comprehensive tax returns. These estimated tax forms underscore the proactive financial planning and compliance efforts required from corporations within different state jurisdictions.

Dos and Don'ts

When managing the South Carolina SC1120-T Tentative Corporation Tax Return form, it’s essential to pay close attention to the details to ensure compliance and avoid potential penalties. Here are key dos and don'ts to guide you:

- Do file the SC1120-T by the due date if you anticipate owing corporate income tax or license fee to avoid penalties.

- Do accurately calculate at least ninety percent (90%) of the total tax due by the original due date to prevent penalties.

- Do attach a copy of the federal extension if no income tax or license fee is anticipated to be due and a federal extension has been granted.

- Do use black ink only when filling out the form to ensure that all information is legible and can be processed efficiently.

- Do include your Business Name, FEIN, and SC File Number on your check to ensure that your payment is correctly applied.

- Don't expect a refund from a tentative return, as refunds are not issued for amounts filed using the SC1120-T form.

- Don't forget to attach a schedule listing the corporations included in the return if filing a consolidated return to ensure the group is eligible to file as such.

- Don't cut or modify the form; submit the entire page as instructed to avoid processing delays.

Meticulously following these guidelines will simplify the process of filing your SC1120-T form, keep you compliant with South Carolina Department of Revenue requirements, and help avoid unnecessary delays or penalties.

Misconceptions

Misconceptions about the South Carolina Form SC1120-T, commonly known as the Tentative Corporation Tax Return, can lead to confusion and errors when it comes to corporate tax filing. Here are nine common misunderstandings and explanations to clarify each one:

- It's a final tax return: A significant misconception is treating the SC1120-T as the final tax return. In reality, it is a tentative return used primarily to request an extension and to estimate the taxes owed.

- Refunds are available: Another error is expecting a refund from this form. The SC1120-T doesn't process refunds; its purpose is to calculate and declare estimated tax owed, not to reconcile taxes over the past fiscal year.

- No penalty for late payment if an extension is filed: Even with an extension request through the SC1120-T, corporations must pay at least 90% of the estimated tax by the original due date to avoid penalties.

- Extension automatically granted upon filing: Some believe that filing the SC1120-T itself grants an extension. However, the extension is conditional and depends on the Department’s approval.

- The form is only for income tax: The SC1120-T also applies to the license fee, not just corporate income tax. This dual purpose is often overlooked, leading to underpayment of dues.

- Savings and Loan Associations need to pay the license fee: In contrast to this belief, the license fee explicitly does not apply to savings and loan associations or banks, highlighting the importance of understanding specific exemptions.

- Consolidated returns don’t require detailed lists: Filing a consolidated return without attaching a schedule listing each corporation included can lead to issues with the Department of Revenue, since detailed lists are mandatory.

- A federal extension is sufficient for state filing: While a properly filed federal extension is acceptable, it is essential to attach a copy of it to the SC1120-T. Assuming state compliance without this key step can result in filing errors.

- There's no minimum license fee: Regardless of the estimated taxes or license fees due, there is a minimum license fee of $25.00. This minimum is often forgotten, leading to underpayment.

Familiarity with these points ensures a smoother and more accurate process when dealing with the SC1120-T, avoiding common pitfalls and enhancing compliance with South Carolina tax requirements.

Key takeaways

Filling out and using the SC1120-T form, which is the Tentative Corporation Tax Return for the State of South Carolina, comes with certain key takeaways that are crucial for ensuring compliance and avoiding potential penalties. Understanding these points can help navigate the process smoothly.

- Timely Extension Requests: Corporations anticipating owing any corporate income tax or license fee must file SC1120-T by the original return due date as a request for an extension of time to file their complete tax return.

- Payment Requirements: Any tax due shown on the SC1120-T form must be paid when filed. This underscores the importance of accurately estimating and remitting the owed amount to avoid interest and penalties.

- 90% Minimum Payment: To avoid penalties, at least 90% of the total tax due must be paid by the original due date. This rule ensures that corporations pay a substantial portion of their tax liability on time, even if they are extending the filing of their complete return.

- Use of Federal Extensions: If no tax or fee is due and a federal extension has been requested, a copy of the federal extension must accompany the South Carolina return if it’s filed within the federally extended period. This provision offers a streamlined process for corporations that are also extending their federal tax filing deadline.

- Consolidated Returns: For corporations filing a consolidated return, a single Tentative Return should be filed, accompanied by a list of all corporations included in this return. It’s important to note that the license fee must be calculated separately for each member but then added together, and the fee cannot be less than $25 per taxpayer.

- Mailing and Documentation: When mailing the SC1120-T, it’s critical to include the corporation's business name, Federal Employer Identification Number (FEIN), and South Carolina File Number on the check. Moreover, using black ink and not cutting the submission form are simple but essential instructions for ensuring the form is processed correctly.

By keeping these key points in mind, corporations can effectively navigate the requirements for filing a Tentative Corporation Tax Return in South Carolina, thereby ensuring compliance and minimizing the risk of penalties.

More PDF Templates

What Is Form 8453 - Offers a pathway for employees hired by eligible employers to declare non-membership in SC's pension plans.

Dhec 4024 Form Printable - The document outlines clear steps for applicants to follow, making the certification process transparent.