Fill Your Sc1120 T Template

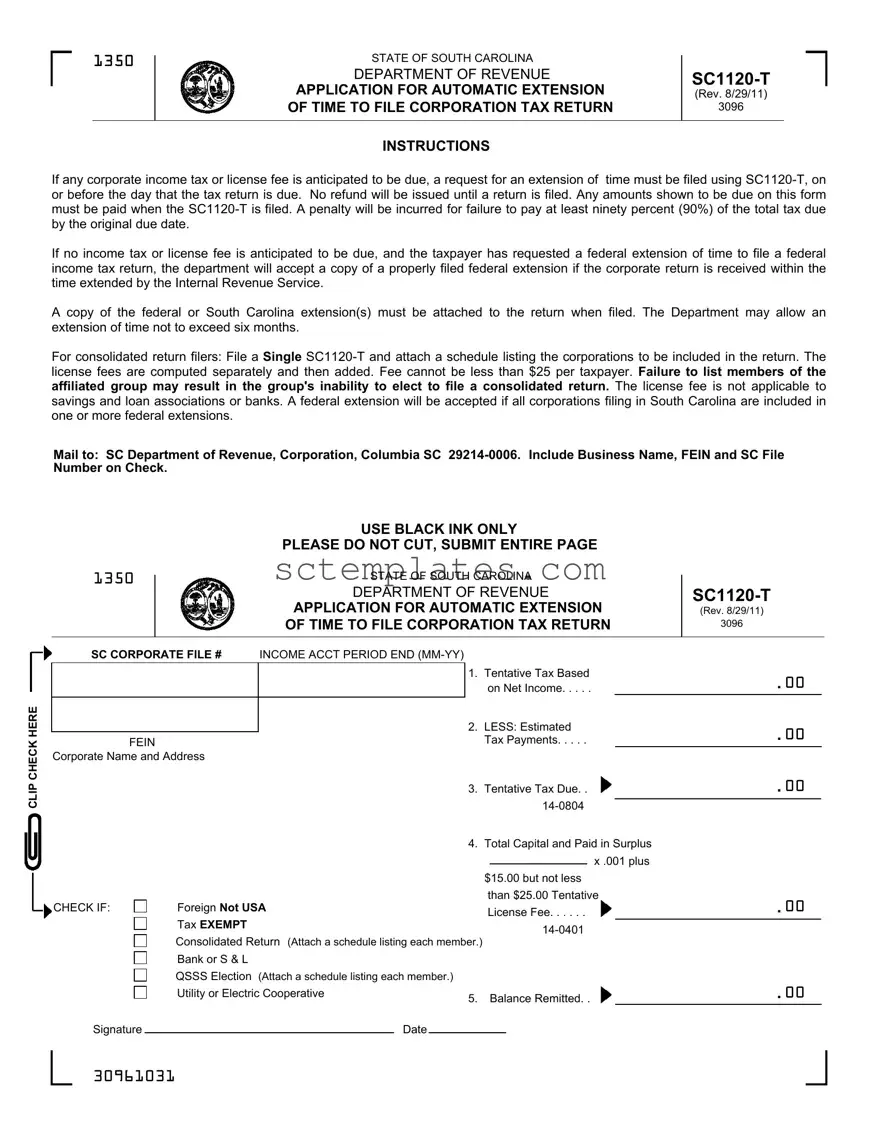

The State of South Carolina Department of Revenue requires corporations operating within its jurisdiction to file the SC1120-T Application for Automatic Extension, a crucial document designed to provide businesses with additional time to file their corporation tax returns. Updated last on August 29, 2011, this form must be submitted on or before the original tax return due date if the corporation anticipates owing any corporate income tax or license fee. The form highlights the condition that any due taxes must be paid concurrently with the filing of the SC1120-T to avoid penalties for underpayment, specifying a minimum of ninety percent (90%) of the total tax due by the original due date to be paid. Notably, for corporations that do not anticipate any tax or license fee liability and have obtained a federal extension, the South Carolina Department of Revenue will recognize a properly filed federal extension, making it essential for the corporate return to be submitted within the extended period granted by the Internal Revenue Service. Additionally, the instructions include stipulations for consolidated return filers, the calculation of license fees, the minimum fee requirement, and the process for including corporations in a consolidated return. The form also details the process for mailing and the necessary information to be provided with payment, hence offering a comprehensive guide for corporations to navigate the extension request process effectively.

Document Example

1350

STATE OF SOUTH CAROLINA |

|

|

|

||

DEPARTMENT OF REVENUE |

||

APPLICATION FOR AUTOMATIC EXTENSION |

||

(Rev. 8/29/11) |

||

OF TIME TO FILE CORPORATION TAX RETURN |

3096 |

|

|

|

INSTRUCTIONS

If any corporate income tax or license fee is anticipated to be due, a request for an extension of time must be filed using

If no income tax or license fee is anticipated to be due, and the taxpayer has requested a federal extension of time to file a federal income tax return, the department will accept a copy of a properly filed federal extension if the corporate return is received within the time extended by the Internal Revenue Service.

A copy of the federal or South Carolina extension(s) must be attached to the return when filed. The Department may allow an extension of time not to exceed six months.

For consolidated return filers: File a Single

Mail to: SC Department of Revenue, Corporation, Columbia SC

CLIP CHECK HERE

USE BLACK INK ONLY

PLEASE DO NOT CUT, SUBMIT ENTIRE PAGE

1350 |

|

|

STATE OF SOUTH CAROLINA |

|

|

|

|||

|

|

|

|

||||||

|

|

|

DEPARTMENT OF REVENUE |

|

|

||||

|

|

|

APPLICATION FOR AUTOMATIC EXTENSION |

(Rev. 8/29/11) |

|

|

|||

|

|

|

OF TIME TO FILE CORPORATION TAX RETURN |

3096 |

|

|

|||

|

|

|

|

|

|

|

|

|

|

SC CORPORATE FILE # |

INCOME ACCT PERIOD END |

|

|

|

|

|

|||

|

|

|

|

Tentative Tax Based |

. |

00 |

|

||

|

|

|

|

1. |

|

||||

|

|

|

|

|

on Net Income |

|

|||

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

LESS: Estimated |

. 00 |

|

|||

FEIN |

|

|

Tax Payments |

|

|||||

|

|

|

|

|

|||||

Corporate Name and Address |

|

|

|

|

|

|

|

||

|

|

|

3. |

Tentative Tax Due. . |

. 00 |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CHECK IF:

CHECK IF:

Signature

4. Total Capital and Paid in Surplus x .001 plus

$15.00 but not less than $25.00 Tentative

Foreign Not USA |

License Fee |

||

|

|

||

Tax EXEMPT |

|||

|

|

||

Consolidated Return (Attach a schedule listing each member.) |

|||

Bank or S & L |

|

|

|

QSSS Election (Attach a schedule listing each member.) |

|

|

|

Utility or Electric Cooperative |

5. Balance Remitted. . |

||

|

|

||

Date |

|

|

|

|

|

|

|

.00

.00

30961031

Form Properties

| # | Fact | Detail |

|---|---|---|

| 1 | Form Purpose | The SC1120-T Form is an application for an automatic extension of time to file corporation tax return in South Carolina. |

| 2 | Due Date | It must be filed on or before the original due date of the corporate tax return. |

| 3 | Payment Requirement | If tax or license fee is due, it must be paid upon filing the SC1120-T. |

| 4 | Penalty for Underpayment | A penalty is applied if less than 90% of the total tax due is not paid by the original due date. |

| 5 | Federal Extension | A properly filed federal extension will be accepted, provided the corporate return is received within the extended time. |

| 6 | Extension Length | The Department of Revenue may grant an extension not to exceed six months. |

| 7 | Consolidated Returns | Only one SC1120-T needs to be filed for consolidated return filers, with an attached schedule listing the included corporations. |

| 8 | Minimum License Fee | The license fee computed cannot be less than $25 per taxpayer. |

| 9 | Exemptions | Banks and savings & loan associations are not subject to the license fee. |

| 10 | Governing Law | This form is governed by the South Carolina Department of Revenue under the state's corporate tax laws. |

Guide to Writing Sc1120 T

For corporations seeking an extension of time to file their South Carolina tax return, the SC1120-T form serves as a vital document. This application facilitates the postponement of filings, either because calculations are yet to be finalized or additional documentation needs to be gathered. The intricacies of this form demand careful attention to detail, ensuring compliance and avoiding potential penalties associated with late or incorrect submissions. Below, a guided approach to completing the SC1120-T form is provided, outlining the necessary steps to ensure accuracy and completeness.

- Start by filling out the corporate name and address in the designated area. Ensure the information matches official records to prevent processing delays.

- Enter the South Carolina Corporate File Number, identifying the specific entity within the state's system.

- Provide the Federal Employer Identification Number (FEIN) to link the state extension with federal records, enhancing coordination between tax authorities.

- Indicate the Income Accounting Period End date (MM-YY), reflecting the fiscal period for which the extension is sought.

- Calculate the Tentative Tax Based on Net Income, entering this amount in the corresponding section. This represents an estimate of the tax liability before deductions.

- Deduct any Estimated Tax Payments already made to arrive at the Tentative Tax Due, ensuring that the total reflects accurate prepayments towards the liability.

- If applicable, compute the Total Capital and Paid in Surplus, multiplying by .001 and adding $15.00, ensuring the minimum fee does not fall below $25.00. This step is crucial for corporations to accurately assess their licensing fees.

- Check the appropriate boxes if the submission pertains to a Tentative Foreign (not USA) License Fee, if the corporation is Tax EXEMPT, or if a Consolidated Return, Bank or S&L, QSSS Election, or Utility or Electric Cooperative designation applies. Attach a schedule listing each member if filing a Consolidated Return or QSSS Election.

- Indicate the Balance Remitted, which is the amount to be paid with the filing of this form. This figure should reflect the tentative tax due after accounting for estimated payments and calculated fees.

- Sign and date the form, certifying the accuracy of the information provided and the compliance with the stated guidelines. The signature validates the request for an extension and authorizes the Department of Revenue to process the application.

- Mail the completed SC1120-T form along with any applicable payment to the South Carolina Department of Revenue, addressing it to the Corporation division in Columbia, SC. It is imperative to include the business name, FEIN, and SC File Number on the check for proper allocation of payments.

By adhering to these instructions, corporations can effectively navigate the complexities of requesting a filing extension, ensuring that all procedural requirements are met. This process, while detailed, provides a systematic approach to maintaining compliance with state tax obligations during periods when extra time is needed to complete and submit corporate tax returns.

Understanding Sc1120 T

What is the purpose of the SC1120-T form?

The SC1120-T form serves as an application for an automatic extension of time to file a corporation tax return in the State of South Carolina. This application is necessary when a corporation anticipates a delay in filing its income tax or license fee and seeks additional time beyond the original due date.

When must the SC1120-T form be filed?

This form must be filed on or before the original due date of the corporate tax return. Filing the SC1120-T form by this deadline allows corporations to avoid penalties by obtaining an extension of time to file their return.

Are there any payment requirements when filing the SC1120-T?

Yes, if any corporate income tax or license fee is anticipated to be due with the return, the estimated amount owed should be paid when the SC1120-T is filed. A penalty will apply if at least ninety percent (90%) of the total tax due is not paid by the original due date.

What if no tax or license fee is due?

If no tax or license fee is anticipated to be due and the corporation has requested a federal extension of time to file its federal income tax return, the South Carolina Department of Revenue will accept a copy of the properly filed federal extension, provided that the corporate return is submitted within the federally extended time frame.

How long can the extension last?

The Department of Revenue may grant an extension of time not to exceed six months from the original filing deadline. This extension is designed to provide sufficient time for corporations to prepare and submit their tax returns without rushing and risking errors.

Is there a minimum fee involved?

Yes, when computing license fees, the amount cannot be less than $25 per taxpayer. This minimum applies to all corporations filing the SC1120-T form and seeking an extension to file their corporate tax returns.

What about consolidated return filers?

Corporations filing a consolidated return must file a single SC1120-T form and attach a schedule listing the corporations to be included in the return. It's important to list all members of the affiliated group correctly, as failure to do so may affect the group's ability to elect to file a consolidated return. Additionally, if a federal extension is accepted, it must include all corporations filing in South Carolina on one or more federal extensions.

Common mistakes

One common mistake is not submitting the payment for the amount due when the form is filed. If the filer anticipates owing any corporate income tax or license fee, it must be paid with the submission of the SC1120-T form. Neglecting this can lead to penalties.

Another error is failing to pay at least ninety percent (90%) of the total tax due by the original due date. This oversight can incur a penalty, adding unnecessary costs to the filer.

Some filers overlook the necessity of attaching a copy of a federal extension if they have requested one and no income tax or license fee is anticipated to be due. This step is critical for the Department to accept the extension.

A critical mistake is not attaching copies of either the federal or South Carolina extension(s) to the return when filed. This documentation is essential for processing.

For consolidations, a common misstep is not including a schedule listing the corporations included in the return. This omission can affect the ability to file a consolidated return properly.

Incorrectly calculating the license fee or not ensuring that it meets the minimum of $25 per taxpayer is another frequent error. Accuracy in calculation is necessary to avoid underpayment penalties.

Failing to notice that the license fee does not apply to savings and loan associations or banks can lead to unnecessary payments or confusion during the filing process.

Omitting the business name, FEIN, or SC File Number on the check used for payment can lead to processing delays or misapplied payments.

Lastly, a significant oversight is using ink other than black to fill out the form, which can cause issues in scanning or processing the document.

Documents used along the form

When preparing to file the SC1120-T form for an automatic extension of time to file a corporation tax return in South Carolina, businesses may need to gather and complete additional forms and documents to ensure compliance and thoroughness in their tax filing process. These additional documents not only complement the SC1120-T but also address various aspects of corporate taxation, license fees, and extensions. Here is a list of documents often used alongside the SC1120-T form:

- SC1120 - South Carolina C Corporation Tax Return: This form is the primary tax return form for corporations operating in South Carolina and is required to report income, deductions, and taxes owed.

- SC1120S - South Carolina S Corporation Tax Return: Required for S corporations, this form reports income, losses, dividends, and taxes owed by S corporations in South Carolina.

- SC1040 - South Carolina Individual Income Tax Return: Shareholders of S corporations and partners in partnerships may need to file this form to report their share of corporation or partnership income.

- SC1065 - Partnership Income Tax Return: Partnerships operating in South Carolina use this form to report their income, gains, losses, and deductions to the state.

- SC8832 - Entity Classification Election: This form is used by entities electing their tax classification as a corporation, partnership, or disregarded entity. It is relevant for determining how an entity is taxed at both state and federal levels.

- SC8453 - Corporate Tax Declaration for Electronic Filing: If the corporation chooses to file their returns electronically, this document is necessary for the declaration and to authenticate the electronic filing.

- SC2210 - Underpayment of Estimated Tax by Individuals, Estates, and Trusts: Corporations expecting to owe $1,000 or more in taxes may need to file estimated tax payments and use this form to determine if they are subject to penalties for underpayment.

- SC2848 - Power of Attorney and Declaration of Representative: Businesses may designate a tax professional or attorney to handle their tax matters with this form, granting them the authority to act on the company's behalf.

This roster of forms and documents aids in conducting thorough and compliant tax preparation for corporations in South Carolina. By understanding and utilizing these documents in conjunction with the SC1120-T, businesses can navigate the complexities of state tax obligations more effectively.

Similar forms

The SC4868 form, which is the Application for Automatic Extension of Time to File U.S. Individual Income Tax Return, shares similarities with the SC1120-T form. Both forms are used to request an automatic extension of time to file tax returns, albeit for different types of taxpayers; the SC4868 is for individuals, while the SC1120-T is for corporations. Each form requires basic information about the taxpayer and an estimate of any tax owed. Moreover, they both emphasize the need to pay any anticipated tax due by the original filing deadline to avoid penalties.

Another document similar to the SC1122-T is the Form 7004, Application for Automatic Extension of Time To File Certain Business Income Tax, Information, and Other Returns. Similar to the SC1120-T, Form 7004 is used primarily by businesses to request more time to file their tax returns. Both forms facilitate an automatic extension, but they cater to different jurisdictions; Form 7004 is for federal tax returns, while SC1120-T is specific to South Carolina. They require information about the tax entity, the tax period, and an estimate of the tax owed.

The SC1041-T form, focusing on trusts and estates within South Carolina, resonates with the function of the SC1120-T but serves a distinct taxpayer group. Like SC1120-T, which provides corporations additional time to file their returns, SC1041-T is used by trusts and estates for similar purposes. Both documents underscore the necessity of estimating and remitting any expected tax liability with the extension request to prevent penalties.

Form 8809, Application for Extension of Time to File Information Returns, also parallels the SC1120-T form in its fundamental purpose of requesting an extension. While the SC1120-T concerns corporate tax returns within South Carolina, Form 8809 is used federally to gain extra time for filing various information returns. Both forms play crucial roles in ensuring accurate and timely tax reporting by providing additional preparation time.

The SC1120S form, specific to S corporations in South Carolina, is akin to the SC1120-T but serves a different phase of the tax filing process. While SC1120-T requests an extension for filing, the SC1122S form is the actual tax return document for S corporations. Both are integral to the tax compliance framework in South Carolina, ensuring that corporations and S corporations, respectively, fulfill their reporting and payment obligations.

Similar in purpose to the SC1120-T is Form 4868, which accommodates individuals looking to extend their federal tax filing deadline. Despite the difference in the taxpayer base, with Form 4868 targeting individuals and SC1120-T focusing on corporations, both offer a mechanism to mitigate late filing through an extension. This shared goal of preventing penalties due to delayed filings underscores their similarity.

The SC1065-T form parallels the SC1120-T in its provision for partnerships in South Carolina seeking an extension to file their returns. Just like the SC1120-T serves corporations, the SC1065-T caters to partnerships that need additional time beyond the original deadline for filing their tax documentation. They both require the estimation of tax due, if any, highlighting the responsibility to comply financially even when filing is delayed.

Lastly, Form 1138, Extension of Time for Payment of Taxes by a Corporation Expecting a Net Operating Loss Carryback, is conceptually similar to the SC1120-T in that it addresses corporate taxation from the angle of extensions. However, Form 1138 is more specialized; it specifically deals with extending the payment deadline based on expected loss carrybacks. Both forms signify the adaptability of tax filing deadlines to corporate fiscal situations, allowing for strategic financial decisions.

Dos and Don'ts

When filling out the SC1120-T form for an automatic extension of time to file a corporation tax return, it's crucial to pay attention to details and follow the instructions carefully. Below is a list of dos and don'ts that will help guide you through the process.

Things you should do:

- Ensure timely filing: File the SC1120-T form on or before the original due date of the corporation tax return to avoid penalties.

- Pay estimated tax due: If you anticipate owing corporate income tax or license fee, pay at least ninety percent (90%) of the total tax due along with the SC1120-T to avoid penalties.

- Include necessary information: Clearly provide the business name, Federal Employer Identification Number (FEIN), and South Carolina File Number on your check when making payments.

- Attach a copy of federal extension: If a federal extension of time to file has been requested and no state tax or license fee is anticipated to be due, attach a copy of the properly filed federal extension to your SC1120-T form.

Things you shouldn't do:

- Delay your filing: Waiting until after the due date to file SC1120-T can result in penalties and interest charges.

- Forget to list affiliated group members: For consolidated returns, failing to attach a schedule listing all corporations included can affect your ability to file a consolidated return.

- Ignore payment of license fees: If applicable, ensure the minimum license fee of $25 per taxpayer is paid, except for banks and savings and loan associations for which the license fee does not apply.

- Use incorrect ink: Do not fill out the form in any ink color other than black to ensure legibility and avoid processing errors.

Misconceptions

When dealing with the State of South Carolina Department of Revenue SC1120-T Application for Automatic Extension of Time to File Corporation Tax Return, several misconceptions can lead to confusion and errors. Understanding the correct information helps ensure compliance and avoids unnecessary penalties. Below are some common misconceptions about the SC1120-T form:

- Misconception #1: Filing for an Extension Gives You More Time to Pay Taxes

This is a common misunderstanding. While the SC1120-T does grant additional time to file the tax return, it does not extend the deadline for any tax payments owed to the state. If taxes are owed, at least 90% of the total tax due must be paid by the original due date to avoid penalties.

- Misconception #2: A Federal Extension Automatically Extends the State Deadline

Many believe that if they have obtained a federal extension, they don’t need to file an SC1120-T. However, while a federal extension can be accepted, a copy of the federal extension must be attached to the corporate tax return or SC1120-T when filed. It is imperative to follow South Carolina's specific procedures to ensure the state extension is granted properly.

- Misconception #3: The SC1120-T Can Be Filed at Any Time Before the Extended Due Date

Filing the SC1120-T requires adherence to deadlines. The form must be submitted on or before the original due date of the tax return. Delaying the filing of SC1120-T can result in the rejection of the extension request and lead to penalties for late filing.

- Misconception #4: There Is No Minimum Fee for Filing

Some taxpayers mistakenly assume there is no cost associated with filing the SC1120-T. However, there is a requirement for a minimum license fee of $25 per taxpayer, irrespective of the tax situation or anticipated refund. This fee is crucial for the successful processing of the extension request.

- Misconception #5: All Corporations Are Eligible for the Same Extension Period

There’s a misconception that all corporations filing an SC1120-T will be granted a uniform six-month extension. The truth is, the Department of Revenue may grant an extension, but the length is not guaranteed. The extension period, up to six months, is evaluated on a case-by-case basis, depending on specific criteria and compliance history.

Dispelling these misconceptions about the SC1120-T form is crucial for businesses aiming to remain compliant with South Carolina's tax obligations. By understanding the form's requirements and deadlines, corporations can more effectively manage their tax filing responsibilities, avoiding penalties and ensuring their financial affairs are in order.

Key takeaways

Understanding how to correctly fill out and use the SC1120-T form is crucial for businesses aiming to file for an automatic extension of time for their South Carolina Corporation Tax Return. Here are key takeaways to ensure compliance and accuracy in the process.

- An extension must be requested by the original due date of the tax return if you anticipate owing corporate income tax or license fees. This is to avoid penalties.

- To avoid penalties, at least ninety percent (90%) of the total tax due must be paid by the original due date.

- If no tax or license fee is due and a federal extension has been filed, attaching a copy of the federal extension will suffice for the state of South Carolina, provided the corporate return is filed within the federally extended time.

- The Department of Revenue may grant an extension not exceeding six months.

- For those filing a consolidated return, a single SC1120-T form should be filed along with a schedule listing all included corporations. Failure to do so might affect the ability to file a consolidated return.

- A minimum license fee of $25 per taxpayer is required, and this fee applies independently to each listed taxpayer.

- Savings and Loan associations or banks are not subject to the license fee.

- When mailing your SC1120-T form, ensure that your business name, Federal Employer Identification Number (FEIN), and South Carolina File Number are clearly indicated on your check.

By adhering to these guidelines, businesses can navigate the extension request process more smoothly, ensuring that all required documentation is submitted correctly and on time. It's important to use black ink and submit the entire page without cutting off any parts to ensure the document is processed accurately.

More PDF Templates

At What Age Do You Stop Paying Property Taxes in South Carolina? - Non-profit community service facilities like soup kitchens or shelters operating without profit motives may qualify for tax-exempt status.

Sc Application State Constable - Personal declarations probe substance use, applications to other government agencies, and membership in organizations potentially conflicting with constable duties.