Fill Your Sc1120S Wh Template

When a business extends beyond the borders of its home state, the financial and regulatory requirements can become significantly more complex, especially in terms of taxation. Among the various forms and obligations, the SC1120S-WH form stands as a critical document for those operating within South Carolina. This form, specifically designed by the State of South Carolina Department of Revenue, targets the withholding tax on income attributed to nonresident shareholders of S corporations. It meticulously outlines how to determine the taxable income for these entities, starting with the South Carolina taxable income and adjusting for directly allocated income. Furthermore, the document provides guidance on calculating the total income allocated to nonresident shareholders and how to account for exemptions to withholding. This includes income exempt by affidavit, composite filing, or due to real estate gains subject to buyer withholding. The completion of this form, crucial for compliance with state tax regulations, requires submission alongside specified documentation to the South Carolina Department of Revenue by a set deadline post the taxable year end. It serves not just as a formality but as a vital component in ensuring that S corporations and their nonresident shareholders meet their tax obligations under South Carolina law. This introduction aims to shed light on the form's major aspects, providing a foundation for understanding both its purpose and its requirements.

Document Example

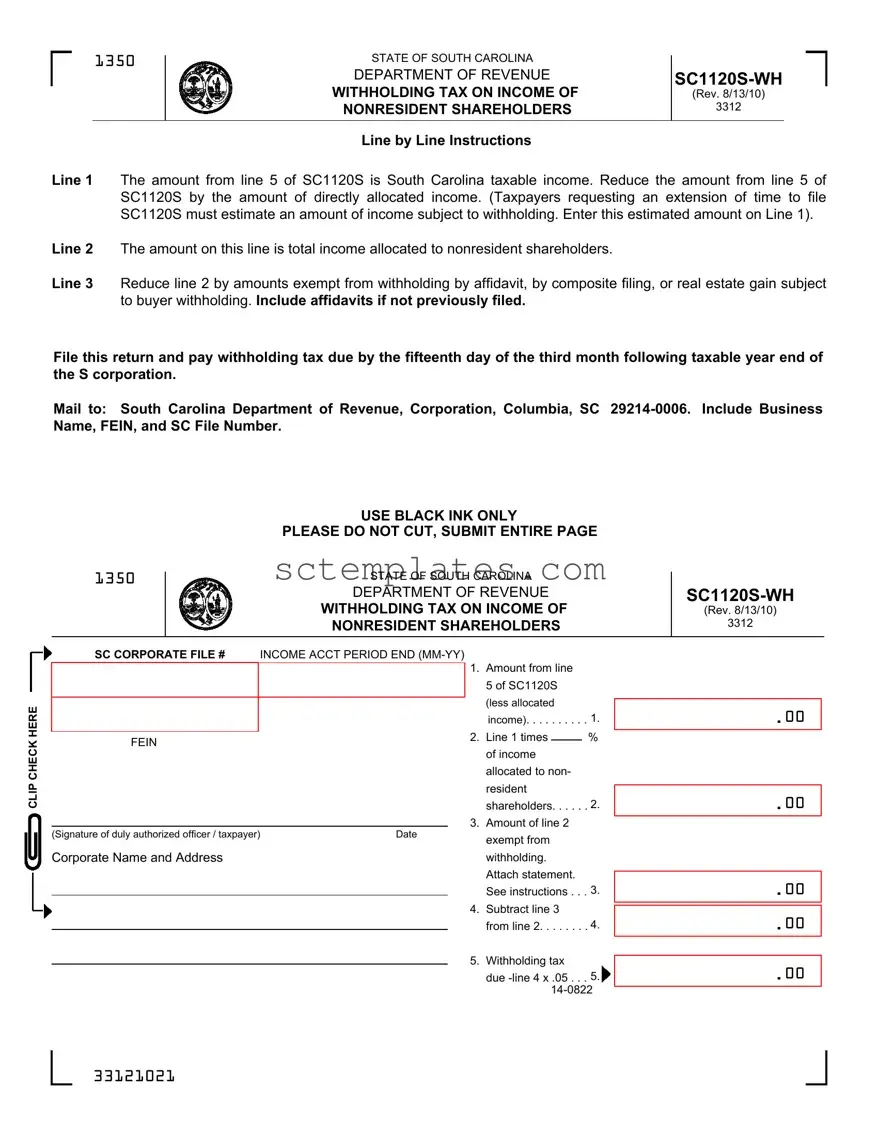

1350

STATE OF SOUTH CAROLINA |

|

DEPARTMENT OF REVENUE |

|

WITHHOLDING TAX ON INCOME OF |

(Rev. 8/13/10) |

NONRESIDENT SHAREHOLDERS |

3312 |

|

|

Line by Line Instructions

Line 1 The amount from line 5 of SC1120S is South Carolina taxable income. Reduce the amount from line 5 of SC1120S by the amount of directly allocated income. (Taxpayers requesting an extension of time to file SC1120S must estimate an amount of income subject to withholding. Enter this estimated amount on Line 1).

Line 2 The amount on this line is total income allocated to nonresident shareholders.

Line 3 Reduce line 2 by amounts exempt from withholding by affidavit, by composite filing, or real estate gain subject to buyer withholding. Include affidavits if not previously filed.

File this return and pay withholding tax due by the fifteenth day of the third month following taxable year end of the S corporation.

Mail to: South Carolina Department of Revenue, Corporation, Columbia, SC

|

|

USE BLACK INK ONLY |

|

|

PLEASE DO NOT CUT, SUBMIT ENTIRE PAGE |

1350 |

|

STATE OF SOUTH CAROLINA |

|

||

|

|

DEPARTMENT OF REVENUE |

|

|

WITHHOLDING TAX ON INCOME OF |

|

|

NONRESIDENT SHAREHOLDERS |

|

|

|

(Rev. 8/13/10)

3312

CLIP CHECK HERE

SC CORPORATE FILE # INCOME ACCT PERIOD END

FEIN

(Signature of duly authorized officer / taxpayer) |

Date |

Corporate Name and Address

1.Amount from line 5 of SC1120S (less allocated

income). . . . . . . . . . 1.

2. Line 1 times % of income allocated to non- resident shareholders. . . . . . 2.

3.Amount of line 2 exempt from withholding. Attach statement. See instructions . . . 3.

4.Subtract line 3

from line 2. . . . . . . . 4.

5.Withholding tax

due

. 00

. 00

. 00

. 00

. 00

33121021

Form Properties

| Fact | Detail |

|---|---|

| Form name | SC1120S-WH |

| Purpose | Withholding Tax on Income of Nonresident Shareholders |

| Revision date | August 13, 2010 |

| Administered by | South Carolina Department of Revenue |

| Due date | 15th day of the third month following the taxable year end |

| Mailing address | Corporation, Columbia, SC 29214-0006 |

| Ink color | Black ink only |

| Exemptions | Reduced by amounts exempt from withholding, including affidavits, composite filing, or real estate gain subject to buyer withholding |

| Governing law | South Carolina State Law |

| Tax rate | 5% |

Guide to Writing Sc1120S Wh

Filling out government forms can often feel complex and overwhelming. The SC1120S-WH form, specifically designed for withholding tax on income of nonresident shareholders in South Carolina, plays a crucial role in ensuring tax compliance for S corporations. Ensuring accuracy while filling out this form is essential, not only to meet legal obligations but also to prevent potential issues with the South Carolina Department of Revenue. Following a step-by-step walkthrough can simplify the process, making it more approachable.

- Start with Line 1: Enter the South Carolina taxable income, which is the amount from line 5 of SC1120S after reducing it by the amount of directly allocated income. For extension requests, enter the estimated amount of income subject to withholding.

- Proceed to Line 2: Calculate and enter the total income allocated to nonresident shareholders.

- For Line 3: Deduct amounts exempt from withholding. This includes income exempted by affidavit, composite filing, or real estate gains subject to buyer withholding. Attach any affidavits if they have not been filed previously.

- Calculate Line 4: Subtract the amount on Line 3 from the amount on Line 2 to find the total income subject to withholding.

- Finally, complete Line 5: Multiply the amount on Line 4 by 0.05 to calculate the withholding tax due. Enter this amount.

Once all the information is accurately entered, review the form to ensure all details are correct. It is important to use black ink and not alter the format of the form, for example, by cutting it. The completed form, along with the payment for the withholding tax due, should be mailed by the fifteenth day of the third month following the S corporation's taxable year end to the South Carolina Department of Revenue, Corporation Section, at the Columbia address provided on the form. Include the business name, FEIN, and South Carolina File Number on the correspondence to avoid any processing delays. Timely and accurate submission of the SC1120S-WH form upholds the tax responsibilities of the corporation and contributes to a fair tax process for all South Carolina residents and businesses.

Understanding Sc1120S Wh

What is the SC1120S-WH form and who needs to file it?

The SC1120S-WH form is a specific tax document required by the State of South Carolina's Department of Revenue. It is designed for the withholding tax on income of nonresident shareholders of an S corporation. This form must be filed by S corporations that distribute income to nonresident shareholders. These corporations are responsible for withholding the tax due on this income and remitting it to the South Carolina Department of Revenue.

How is the income subject to withholding calculated on the SC1120S-WH form?

The income subject to withholding is calculated by starting with the South Carolina taxable income from line 5 of SC1120S and reducing this amount by any directly allocated income. The S corporation must estimate the income that will be subject to withholding if requesting an extension of time to file SC1120S and enter this estimated amount on Line 1 of the SC1120S-WH form. This forms the basis for the calculation of the withholding tax due.

What is total income allocated to nonresident shareholders?

Total income allocated to nonresident shareholders refers to the portion of the S corporation's income that is distributed to or allocated for its shareholders who are not residents of South Carolina. This amount is reported on Line 2 of the SC1120S-WH form. It includes all income before any exemptions or deductions related to withholding are applied.

How can an S corporation reduce its withholding obligation?

An S corporation can reduce its withholding obligation for nonresident shareholders by subtracting from its total income allocated to nonresident shareholders (Line 2) any amounts that are exempt from withholding. Exemptions can be due to the submission of an affidavit by the shareholder, composite filing, or because the gain is from real estate subject to buyer withholding. The corporation should attach any required affidavits if they have not been previously filed. The net amount after these deductions is used to calculate the withholding tax.

When is the SC1120S-WH form due?

The SC1120S-WH form must be filed and the appropriate withholding tax paid by the fifteenth day of the third month following the taxable year-end of the S corporation. This deadline ensures that the S corporation remains in compliance with South Carolina's taxation requirements and avoids potential penalties for late filing and payment.

Where should the SC1120S-WH form be mailed?

The completed SC1120S-WH form, along with any payment due for withholding tax, should be mailed to the South Carolina Department of Revenue at the address specified on the form: Corporation, Columbia, SC 29214-0006. It is important that the S corporation includes its business name, FEIN (Federal Employer Identification Number), and South Carolina File Number when submitting the form to ensure proper processing and credit of the payment.

Common mistakes

When filling out the SC1120S-WH form, it’s essential to approach it with care to ensure compliance with tax requirements for nonresident shareholders. Mistakes can lead to penalties, delays, and additional scrutiny from the South Carolina Department of Revenue. Here are common missteps to avoid:

- Not reducing the taxable income by directly allocated income. It's crucial to adjust the amount from line 5 of SC1120S by the amount of directly allocated income.

- Estimating the income subject to withholding inaccurately when requesting an extension can lead to incorrect withholding amounts, underpayment, or overpayment.

- Failing to correctly calculate the total income allocated to nonresident shareholders. This calculation forms the basis for determining the withholding tax and must be accurate.

- Omitting exempt income reductions such as those by affidavit, by composite filing, or by real estate gain subject to buyer withholding. This oversight could result in overpaying tax.

- Not including necessary affidavits if they haven’t been previously filed. These documents are essential for verifying exemptions claimed on the form.

- Using ink other than black to fill out the form may seem trivial but is explicitly stated in the instructions and could lead to processing delays.

- Ignoring the due date for filing the return and paying the withholding tax (the fifteenth day of the third month following the taxable year-end) can result in penalties and interest charges.

- Overlooking the need to include the Business Name, FEIN, and SC File Number. These identifiers are crucial for processing the form and ensuring the correct application of payments.

Avoiding these mistakes will help ensure that the SC1120S-WH form is filled out correctly and in compliance with South Carolina’s withholding tax requirements on nonresident shareholders' income.

Documents used along the form

When dealing with the SC1120S-WH form, a key document for handling withholding tax on income of nonresident shareholders in South Carolina, it's essential to be aware that this is often just one piece of the puzzle. To ensure full compliance and optimal handling of a corporation's tax obligations, a variety of additional forms and documents are commonly used alongside the SC1120S-WH. Each document serves its purpose, providing detailed information or fulfilling specific legal requirements for the corporation.

- SC1120S - This form is the South Carolina S Corporation Income Tax Return. It is the core document where the S corporation reports its income, gains, losses, deductions, and credits. The information on this form is used to determine the amount on line 5 of the SC1120S that is referenced in the SC1120S-WH form.

- W-9 - Request for Taxpayer Identification Number and Certification. This form is often collected from nonresident shareholders to ensure their correct taxpayer identification numbers (TINs) are on file, which are necessary for reporting and withholding purposes.

- 2848 - Power of Attorney and Declaration of Representative. This form allows a representative to act on behalf of the corporation or shareholder in tax matters, providing the legal authority to handle such affairs.

- W-4 - Employee's Withholding Certificate. While primarily for employees, a version of this form may be used by corporate shareholders in certain contexts to determine the correct amount of tax withholding from distributions or income.

- K-1 (Form 1120S) - Shareholder's Share of Income, Deductions, Credits, etc. This document outlines each shareholder's proportion of the income and losses, which influences their individual tax liabilities, including the calculation for nonresident withholding taxes.

- 8832 - Entity Classification Election. This form might be relevant for entities that have a choice in how they are taxed (corporation, partnership, or disregarded entity) and can affect how income and withholdings are reported.

- SS-4 - Application for Employer Identification Number (EIN). This form is essential for any corporation, including S corporations, needing an EIN for tax purposes, which is required on the SC1120S-WH form.

- 4868 - Application for Automatic Extension of Time To File U.S. Individual Income Tax Return. Even though it is for individuals, similar forms for businesses allow for extensions on filing returns, affecting when withholding taxes need to be calculated and paid.

- Estimated Tax Payments - Corporations, including S corporations, may need to make estimated tax payments quarterly. While not a single form, this process requires keeping track of payments due and ensuring that they are made on time to avoid penalties.

Understanding and managing these documents in conjunction with the SC1120S-WH form can streamline the tax handling process for nonresident shareholders and the corporation itself. These documents collectively ensure that all aspects of income and withholding tax compliance are addressed, maintaining the corporation's good standing and supporting accurate financial reporting. Navigating through these forms with a meticulous approach benefits not only the corporation but also its shareholders, ensuring regulatory compliance and financial health.

Similar forms

The SC1120S form, used for reporting South Carolina taxable income and allocating income to nonresident shareholders, shares similarities with the 1041 U.S. Income Tax Return for Estates and Trusts. Both forms involve the calculation and reporting of income, as well as the potential for allocating earnings to various parties. The 1041 form requires estates and trusts to report income, deductions, and credits to the IRS. Just like the SC1120S-WH mandates specific documentation for nonresident shareholders, the 1041 form demands detailed information about the beneficiaries of the estate or trust, including their share of the income.

The W-2 Form, which is used by employers to report wages, taxes withheld, and other compensation to employees, also shares some common procedures with the SC1120S-WH. Both forms involve reporting to a tax authority and require detailed financial information. While the SC1120S-WH focuses on income from nonresident shareholders and the related withholding tax, the W-2 captures employee earnings and the tax withheld from those earnings. Despite their differences in audience and purpose, the essence of reporting specific income types and withholding taxes binds them closely.

Another document that parallels the SC1120S-WH is the Form 1099-MISC, used for reporting miscellaneous income. Similar to the SC1120S-WH, which deals with income allocation for nonresident shareholders, the 1099-MISC is intended for reporting payments made in the course of a trade or business to non-employees. Both forms play crucial roles in ensuring proper reporting and taxation of income, although they cater to different recipients – the SC1120S-WH focuses on shareholders, while the 1099-MISC is broader, including contractors and other non-employees.

The K-1 Form, another document linked to partnerships and S corporations, closely resembles the SC1120S-WH in its function of allocating income to owners or shareholders. The K-1 Form is essential for reporting each shareholder’s share of the business's earnings, losses, deductions, and credits. Like the SC1120S-WH, which allocates South Carolina taxable income to nonresident shareholders, the K-1 ensures that each entity or individual pays tax on their portion of the earnings, making both forms pivotal for accurate tax reporting and compliance.

Lastly, the 8825 Form, used by partnerships and S corporations to report income and expenses from rental real estate, exhibits similarities to the SC1120S-WH form. While the 8825 focuses on rental real estate income, both forms require detailed financial reporting and can involve allocating income to various parties. Like the SC1120S-WH aims to allocate and withhold tax for nonresident shareholders accurately, the 8825 is concerned with portraying the financial aspects of real estate under the entity’s control. Both play significant roles in the financial reporting and taxation processes of their respective entities.

Dos and Don'ts

Filling out the SC1120S-WH form, which is the Withholding Tax on Income of Nonresident Shareholders in South Carolina, requires careful attention to detail to ensure compliance. Here are guidelines on what you should and shouldn’t do during the process:

- Do ensure that all information is accurate, especially the amount from line 5 of the SC1120S, which is the South Carolina taxable income.

- Do not forget to reduce the amount from line 5 of SC1120S by the amount of directly allocated income to get accurate figures.

- Do include an estimated amount of income subject to withholding if you are requesting an extension of time to file SC1120S. This estimate should be entered on Line 1.

- Do not overlook reductions on line 2 for amounts exempt from withholding due to affidavits, composite filings, or real estate gains subject to buyer withholding. Make sure these reductions are applied before calculating the withholding tax due.

- Do attach any required affidavits if they have not been filed previously, to comply with exemptions from withholding.

- Do ensure presentations are made timely; file this return and pay the appropriate withholding tax by the fifteenth day of the third month following the taxable year end of the S corporation.

- Do use black ink only and submit the entire page without cutting it, as per the instructions, to maintain the readability and proper handling of your document.

- Do not forget to include your Business Name, FEIN, and SC File Number when submitting the form. These details are crucial for proper filing and identification of your return.

By following these guidelines, you can navigate through the SC1120S-WH form filling process more smoothly and ensure your compliance with South Carolina’s tax requirements for nonresident shareholders. Always double-check your entries and calculations to prevent any errors that could lead to unnecessary delays or complications with your filing.

Misconceptions

When dealing with the SC1120S-WH form, which pertains to withholding tax on income of nonresident shareholders in South Carolina, several misconceptions can lead to misunderstandings or mistakes in compliance. Let's debunk six common myths to ensure accuracy and clarity.

Myth 1: All income is subject to the same rate of withholding. This is not the case; the requirement is to withhold taxes only on the allocated income to nonresident shareholders after certain reductions, such as directly allocated income or amounts exempt due to specific conditions like affidavits or composite filings.

Myth 2: Extensions for filing the SC1120S also apply to the SC1120S-WH by default. While taxpayers may request an extension for the SC1120S, it's important to note that estimating the income subject to withholding and entering this amount on Line 1 must still be done timely. The due date for the SC1120S-WH is not automatically extended with the SC1120S.

Myth 3: Real estate gains are always subject to withholding for nonresident shareholders. In fact, real estate gains can be exempt from withholding if subject to buyer withholding, showing the importance of reducing the total income allocated on line 2 by these and other exempt amounts.

Myth 4: Withholding tax is optional for nonresident shareholders. Quite the contrary, it is a mandatory procedure for S corporations with nonresident shareholders, ensuring part of their income tax obligations in South Carolina are pre-paid.

Myth 5: Withholding tax documents need to be mailed with colored ink or special paper. The instructions specify the use of black ink explicitly and instruct not to cut the form, highlighting the state's requirements for consistency and legibility.

Myth 6: Affidavits and other exemptions don't need to be filed if they were previously submitted. The SC1120S-WH instructions highlight the necessity of including affidavits if they were not previously filed, indicating that up-to-date documentation must accompany the withholding tax filing.

Understanding these misconceptions and the actual requirements of the SC1120S-WH form can guide S corporations and their nonresident shareholders toward compliant and efficient tax filings in South Carolina, avoiding unnecessary penalties or delays. Always ensure that the most current form and instructions are being followed, as tax laws and regulations may change.

Key takeaways

Navigating the SC1120S-WH form can be straightforward with the right guidance. Here's what you need to know to fill it out and use it properly:

- Understanding the Purpose: The SC1120S-WH form is specifically designed for the withholding tax on income of nonresident shareholders of S corporations in South Carolina. This is crucial for ensuring compliance with state tax obligations.

- Identifying Taxable Income: The amount on line 5 of the SC1120S form represents the South Carolina taxable income. It's essential to start with this figure to determine the initial base for any withholdings.

- Adjustment for Direct Allocation: Directly allocated income must be subtracted from the taxable income total on line 5 of SC1120S. This adjustment is vital for accurately determining the income subject to withholding.

- Estimating Income for Extension Requests: If requesting an extension for filing the SC1120S, an estimated income figure subject to withholding needs to be entered on Line 1. Accuracy in these estimates helps in avoiding underpayment penalties.

- Allocating Income to Nonresident Shareholders: Total income allocated to nonresident shareholders is outlined on line 2. This step is fundamental for understanding the portion of income that could be subject to withholding.

- Exemption Considerations: Not all allocated income is subject to withholding. Line 3 allows for the reduction of exempt income, such as that covered by affidavit, composite filing, or related to real estate gain subject to buyer withholding. Accurate exclusion of these amounts ensures that overpayment of taxes is avoided.

- Filing Deadline and Payment: The form and related withholding tax due must be filed and paid by the fifteenth day of the third month following the taxable year end of the S corporation. Timeliness is critical to prevent penalties and interest for late submission.

- Mailing Instructions: When submitting the form, include the business name, FEIN, and SC File Number. Use black ink and avoid modifying the form size. Proper submission ensures timely processing and avoids delays.

By keeping these key points in mind, filling out and submitting the SC1120S-WH form can be a seamless process. Focus on the details, meet the deadlines, and ensure compliance to support the financial health and legal standing of your S corporation in South Carolina.

More PDF Templates

South Carolina Corporate Income Tax Return - The form must be completed with care to avoid penalties for inaccurate or incomplete submissions, indicating the legal responsibility of filing accurately.

South Carolina Sit - The form facilitates compliance with state tax laws by detailing the sale's specifics, including gain and withholding amounts.

How Long Is a Tb Test Good for Teachers - This document also assists in identifying individuals who may pose a risk of TB transmission in schools and daycare centers.